Portfolio Manager Summary

AudioEye (AEYE) is a software-as-a-service (SaaS) company that provides website accessibility compliance – in plain English, it claims to use machine learning/AI to ensure that clients’ websites comply with web content accessibility guidelines (WCAG), specifically as they pertain to individuals with disabilities.

From the lows in March, AEYE’s stock is up ~585% – key highlights of the bull thesis include AEYE’s recent performance in certain financial metrics and expected potential catalysts for the stock – for both 1Q and 2Q 2020 the company beat analyst revenue and EBITDA expectations. The company’s monthly recurring revenue (MRR) also increased 104% in Q1 and 105% in Q2 compared to the same period last year. Since the end of 2019, the company’s customer count has gone from 6,800 customers to over 20,000. B. Riley recently upgraded its price target to $25 from $21 citing what has been a common theme among retail investors which is: “the pandemic-driven shift toward digital channels that could serve as a medium-term tailwind for web accessibility adoption”.

While these factors have pushed the stock price up, we believe, at its core, the business remains unchanged. To capitalize on such momentum and be successful, a company needs good management, strong investment in innovation, a strong product and various other factors. In this article we delve into what we believe are serious issues with AudioEye, and why we think it lacks in all these areas, posing a great risk to shareholders.

AEYE has the following:

- Founding team has experience starting businesses that seemingly go nowhere. Many of these businesses have engaged in related party deals and have been alleged pump and dumps, one of which was halted by the SEC and down 82%

- Founder Nathaniel Bradley’s latest venture is Parallax (OTC: PRLX) which was recently halted by the SEC because of the accuracy of the claims made by the company regarding its COVID-19 test

- At one point, “Pharma Bro” Martin Shkreli was a significant shareholder in AEYE. The connection to Shkreli continues to this day, as the current CEO was previously involved with Shkreli’s effort to revive KaloBios

- We believe AEYE already has weak governance – but further questions are raised when we investigate the background of another board member who sat on the board of another company with big promises that ended in bankruptcy

- The product category has been looked upon skeptically as automated accessibility remediation might not be the best solution

- For a company that claims to be innovative within their field, AEYE has spent minimally on R&D. Their R&D spend as a percent of revenue is well below the SaaS company median and nominally does not justify its valuation or claims of valuable IP

- Our research suggests that AudioEye’s financials should be looked at with the highest amount of skepticism. Their auditor appears to have a pattern of serious PCAOB deficiencies and was charged by the SEC for improper professional conduct

- The company has amended and reclassified historical financials (and at one point restated 97% of its revenue) likely enabled or caused by material weaknesses in internal controls

Because of these considerations, we believe that AEYE’s prospects are no better than they were before the stock started running in April, and assign an $8 price target to the stock, down ~50% from the last close.

Founders’ unusual entrepreneurial histories

AudioEye was allegedly founded in 2005 as “an R&D company” by a group including the company’s current SVP of Customer Advocacy and former President, Sean Bradley. Sean and his brother, Nathaniel (the former AEYE CEO through 2015), are prolific entrepreneurs, having started or run several entities alongside James Crawford and David Ide – Kino Digital, Kino Communications, Kino Interactive, Modavox, Augme, and Hipcricket.

Rather than run these companies privately, it appears that Nathaniel Bradley and his crew enjoyed listing them on the OTC markets – both Modavox and Augme were pink sheet companies, as is his current venture, Parallax (OTC: PRLX).

Curiously, the Kino/Modavox/Augme ecosystem not only had this group of people in common, but it also culminated in series of related party acquisitions, as helpfully explained by James Crawford:

So Modavox bought Kino and Augme, and Augme purchased Hipcricket in 2011 for an eye popping $45MM, and rebranded the entire company Hipcricket. Unfortunately for all parties involved, Hipcricket filed for bankruptcy in 2015, and its assets were acquired by SITO Mobile for just $5MM, just over 10% of what Augme paid back in 2011.

Perhaps it is reasonable to say that the Bradley brothers are better at starting companies than running them, and we view Sean in a leadership seat at AEYE as a significant red flag.

If that weren’t enough, the SEC recently halted trading of Nathaniel Bradley’s Parallax Health Sciences, “because of questions regarding the accuracy and adequacy of information in the marketplace. Those questions relate to statements Parallax made about its purported development of a rapid screening test for COVID-19 and its purported access to large quantities of COVID-19 diagnostic testing kits and personal protective equipment” Since the beginning of 2019, Parallax’s stock is down 82% – not a rousing endorsement for companies in Bradley’s world.

One of AEYE’s other founders, David Ide, is worth a deeper look – in addition to founding AEYE, Ide claims to have founded Spindle Mobile, Spindle, Inc and sits on the board of SEFE and GlyEco:

- In 2012, SEFE spiked from approximately 80c to $2.20, before utterly collapsing 98% to close the year at just 5c

- Between September 2013 and March 2014, Spindle Inc. rallied approximately 368%, only to collapse 93% to just 24c by September 2014 – the stock was recently halted at $0.003

- GlyEco appears to have suffered the same fate as SEFE and Spindle – it has gone from mid-teens in 2017 to just 3c today

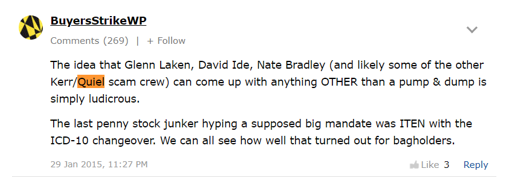

Now if this has you thinking, “are these pump and dumps?” – maybe you’re on to something. We’ve seen several posts critical of SEFE and the people involved, Ide included, but this Seeking Alpha comment really caught our eye:

While we readily admit that neither Nathaniel Bradley and David Ide are involved in AEYE today, their troubling past activities cause us to cast a skeptical eye on anything AEYE does. And that is just the beginning of this story. Later we’ll dig into the auditor, product and investment in the company’s future.

A troubled ‘Toosie Slide’: we believe that repeated reshuffling at the executive level is concerning

In April 2015, Nathaniel Bradley resigned as CEO and President of AEYE, coinciding with the company’s announcement that it needed to restate certain financials (more on that later). His brother, Sean, was moved to the President role, and Nathaniel was inexplicably kept on as Chief Innovation Officer and Treasurer. James Crawford also resigned as COO and Treasurer.

In November that year, Todd Bankofier was named CEO, remaining there until he was apparently demoted to Chief Revenue Officer in September 2019, when executive chairman Carr Bettis stepped in as interim CEO. Then, in January 2020, what we would assume to be an unhappy Bankofier notified the company of his resignation.

Just two short months later, AEYE announced the appointment of Heath Thompson as CEO, with Bettis quoted: “Heath has a decorated past in leading technology and specifically SaaS business model transformations. In Heath, we found a leader who possesses the skills that we were looking for to execute on AudioEye’s long-term growth plans. We are looking forward to leveraging Heath’s track record and unique skill set to take advantage of the rapidly growing market opportunity for our products and technology.”

And then, barely five months later, we learn that Heath Thompson has moved away from the CEO role into a “strategic advisor” position. Does this mean Heath is even employed at AEYE? What could he have experienced that would make him step down as CEO in such short order?

A “Pharma Bro” Shkreli associate takes over as CEO

Upon Heath Thompson’s departure, David Moradi, who joined the board in 2019, took over as CEO. Moradi is the Founder and Manager of Sero Capital, LLC, a Miami Beach-based entity that owns approximately 28% of AEYE. Moradi, like the Bradley brothers before him, has an “interesting” background.

In November 2015, “Pharma Bro” Martin Shkreli and other investors took a majority stake in OTC-listed KaloBios, a CA-based biopharmaceutical company, in an effort to revive the company’s leukemia drug. The other investors here included one David Moradi, who was elected to the board of KaloBios. KaloBios eventually filed for bankruptcy in December 2015 and terminated Shkreli as its CEO when he was arrested, and has since been restructured as Humanigen (OTC: HGEN).

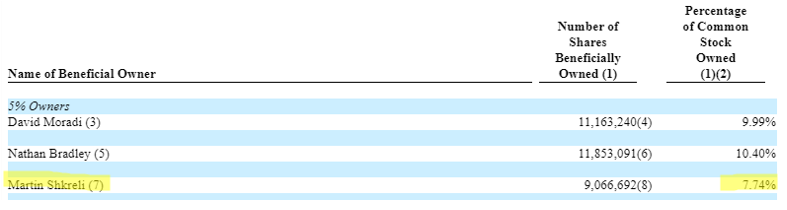

Moradi and Shkreli do appear to work together in more ways than one, since Shkreli himself owned 7.7% of AEYE at the end of 2016:

On top of being connected through Moradi, one of the Directors who resigned very recently was also involved in KaloBios. Alexandre Zyngier (LinkedIn), lists himself as the Founder of Batuta Capital Advisors. This same firm is named in a bankruptcy document as the financial advisor to KaloBios. He served on the board of Audio Eye from October 2015 to July 2020.

We view these relationships as significant red flags, as Martin Shkreli was convicted of securities fraud charges in 2017.

And if this were not enough, AEYE has Marc Lehmann on its board – for those of you not familiar with Marc, he has a sterling resume with degrees from NYU and Wharton, and stints at Appaloosa, SAC, and JANA Partners.

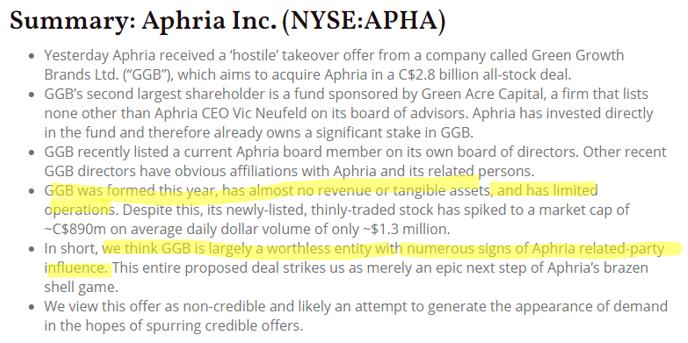

This would be well and good for AEYE, but unfortunately Marc was also a director at Green Growth Brands (GGB), a Canadian cannabis company. GGB was critically evaluated as a hostile suitor for Aphria by Hindenburg Research, who characterized GGB as follows:

Hindenburg’s commentary was prescient, as GGB filed for bankruptcy protection in May 2020, after it faced a “severe liquidity crisis”. We tip our hat to Hindenburg Research for their work here.

We would question the judgment and intentions of anyone who would sit on a board of a company like GGB, and view Marc’s presence on the AEYE as a red flag.

This, combined with Moradi and Zyngier’s apparent Shkreli affiliation, Heath Thompson’s surprisingly short tenure, and the Bradley brothers’ track record, causes us to question management’s claims and credibility. These are by no means dispositive of untoward activity, but we view them as significant red flags and risks to shareholders.

We believe the questionable business practices of management have planted their seeds within the company. A pattern of product and technology reshuffles combined with negative industry commentary about the product category suggests that investors may be expecting too much from too little.

AEYE’s evolving product suite

AEYE, despite being incorporated in Delaware in 2005, actually goes back a bit further – it was started in 2001 as a product which allowed “site owners convert any text-based web site into an intuitive, mirrored audio format” so that users could “navigate the internet solely by listening to Streaming Audio prompts and performing simple keystroke commands from any internet-enabled device”.

By 2005, AEYE was marketing itself as a social entrepreneurship venture:

“The development of AudioEye reflects our core values of social entrepreneurship. The company was founded as a private market solution to an important public policy problem. Many learning-disabled, visually impaired, elderly, young children, non-English speakers, and sighted individuals are faced with a low quality Internet experience. It is improving everyday, but we believe AudioEye can open many doors for those left behind by the first Internet revolution”

By 2011, AEYE had decided it had been founded in 2003 and billed itself as a developer of “Internet content publication and distribution software that enables conversion of any media into accessible formats and allows for real time distribution to end users on any Internet connected device”, adding several new products to its existing audio platform:

- An emergency alert system that claimed to deploy instant alerts to a community of subscribers

- “E-Learning” systems “accessibility at the forefront”

- The IF Factory – “Internet Factum (Factum: do everything) offers a specific accessible product line including internet pay-per-view, mobile, enterprise broadcasting, accounting venue and event based technology products”

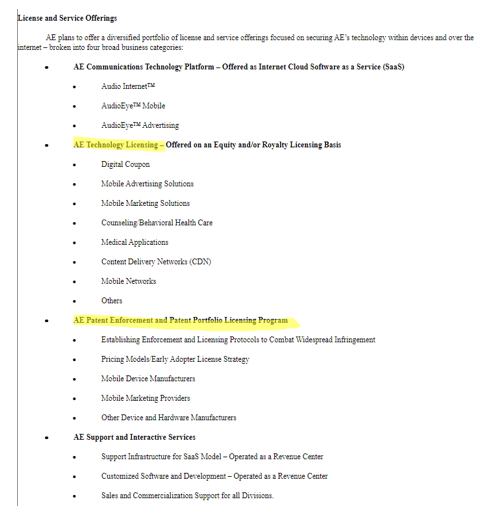

By 2013, AEYE had added new lines of business – licensing and patent enforcement:

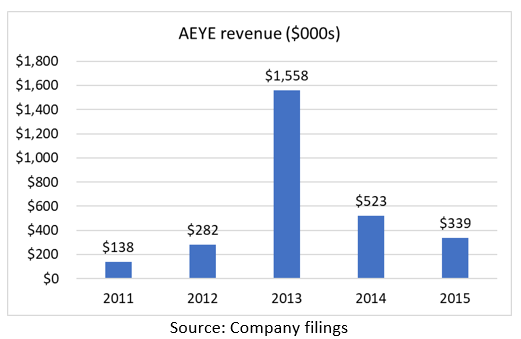

None of these alterations and products seems to create a sustainable revenue stream, with revenues peaking in 2013 and falling 78% to a nadir of $339k in 2015:

Then, after spending an average of just $443k per year in R&D in 2014, 2015, and 2016, we have essentially what AEYE pitches as its product set today – an “always-on, proprietary machine-learning/AI-driven technology automatically identifying and resolving the most common WCAG accessibility errors (approximately 35-percent) coupled with AudioEye’s team of digital accessibility subject matter experts monitoring, manually testing and resolving the remaining errors.”

But, according to our research, it doesn’t seem like website accessibility software packages are as easy to deploy or as effective as the players in the industry would like you to believe.

The first product review that shows up on Google for AEYE is from Kris Rivenburgh, the Chief Legal Officer and Chief Accessibility officer of Essential Accessibility and an expert on website accessibility compliance, who reviewed AEYE’s products and came to following conclusions:

“AI hasn’t come very far with accessibility”

The best automated scans only flag ¼ of accessibility issues (AEYE claims 35%!)

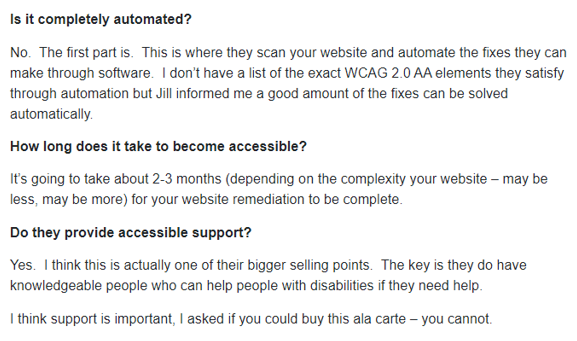

What Kris implies is that true website compliance only happens with manual reviews and testing of the code, as confirmed by his conversation with an AEYE salesperson:

The second review, from whoisaccessible.com, ranks AEYE at the top of their product reviews with a score of 4.7 out of 5, with an overwhelmingly positive assessment:

Even this review, however, cites the difficultly of automated compliance:

Whoisaccessible.com provides links to receive quotes from the accessibility providers that it reviews, and in its fine print discloses that it may receive compensation through affiliate program for the products reviews on its site:

Searches on Reddit found conclusions similar to Rivenburgh’s:

A Reddit thread titled “Questions for AudioEye buyers and users” asks about the reasons behind using AEYE as well as perceived user experience:

Some of the responses are insightful as to the difficulty successfully achieving website compliance as well as the decision to market the products as mitigating legal risk vs actually helping disabled users:

100% compliance is only achieved by changing code

Why do people sign up for WCAG compliance?

Significant skepticism from a reviewer

“Technical individuals in all sectors that understand that these solutions are nonsense”

“We’re simply not there yet”

Another thread, about competitor AccessiBe, has similar commentary about the product category:

“…I found their claims to be ridiculous. The same is true for AudioEye, UsableNet, and more.”

A June 2020 piece critical of AccessiBe’s product goes further, saying:

R&D spend appears to lag industry median, nominal spend doesn’t appear to get it done

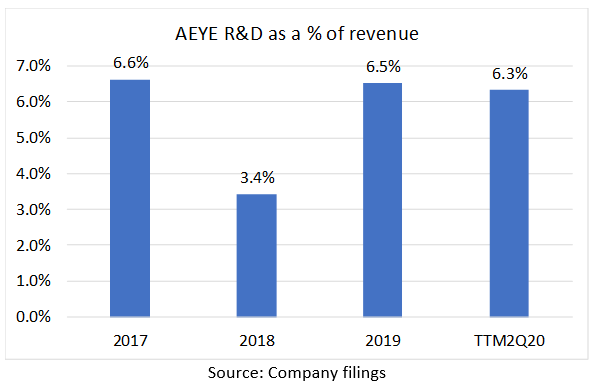

For a company that claims its roots as an “an R&D company”, AEYE appears to spend much less on R&D than the average SaaS company. A 2018 review of public SaaS company R&D spend by Sammy Abdullah of Blossom Street Ventures found that “SaaS companies spent on median 23% of revenue on R&D”, with “the 10 smallest companies by revenue spent 41% of revenue on R&D”.

AEYE, on the other hand, has spent just $3MM in R&D from 2011 to 2Q20 on $32.5MM in revenue, or just 9.4%. While R&D as a % of revenue exceeded 100% in 2014 and 2015, from 2017 onwards it has averaged just 5.7%:

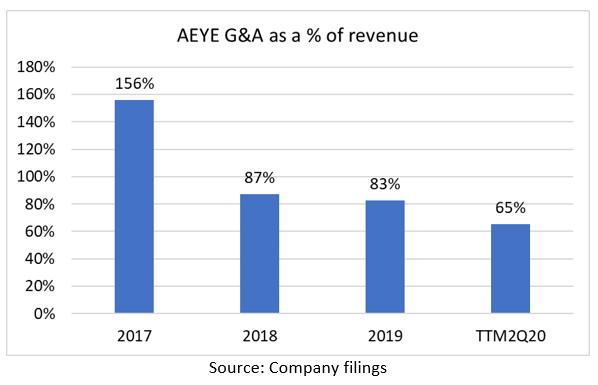

Curiously, what AEYE does spends on is G&A – since 2017, AEYE has spent 81% of its revenues on G&A:

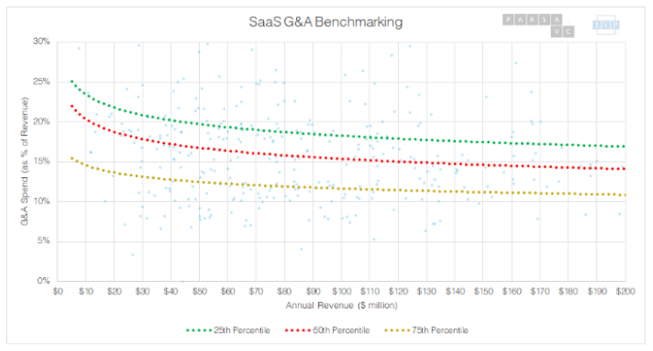

To put this in context, a study of SaaS operating expenses shows that the average SaaS company (the 50th percentile) with AEYE’s approximate revenues, spends a little less than 20% of its revenues on G&A:

Where is all this G&A going? Well, a quick look at the proxies and 10-Ks shows that the named executives, including board chairs, have received total compensation equal to 48% of AEYE’s revenues from 2012 to 2019. Sean Bradley, the only remaining member of the founding team left at AEYE, has emerged the winner – from 2012-2019, Sean received $2.2MM in total compensation, or an eye-popping 9.8% of AEYE’s revenues during the same period.

This rather stark difference between AEYE’s R&D and G&A spend as a percentage of revenue compared to SaaS peers is troubling, in our opinion, as it suggests that management has been and continues to enrich itself at the expense of developing cutting-edge products.

From this, Mariner gathers that:

- Accessibility compliance is hard to achieve with an automated solution

- Current providers of the solutions are focused on mitigating legal risk rather than enhancing usability

- These providers are likely overstating their claims and value add, given the difficulties outlined above

Despite these product and category concerns, AEYE has seen its operating metrics and revenue improve. In the next section, we raise issues that should cause investors to stop and question AEYE’s impressive results – we found an alarming and material restatement, weak internal controls, and a questionable auditor.

Is AEYE’s 2015 restatement the tip of the iceberg?

In 2015, AEYE announced a restatement for:

“…its quarters ended March 31, June 30 and September 30, 2014. The Audit Committee also authorized an internal review of controls and policies. Accordingly, investors should no longer rely upon the Company’s previously released financial statements or other financial data for these periods, including any interim period financial statements, and any earnings releases relating to these periods. In addition, investors should no longer rely on the preliminary earnings release issued by the Company on January 12, 2015 relating to the quarter and year ended December 31, 2014.

Based on the review to date, the Company anticipates removing all revenue derived from non-cash exchanges of a license of the Company for the license of the Company’s customer and all revenue from non-cash exchanges of a license of the Company for services of the Company’s customer, and reducing by a material amount previously reported license cash revenue. The aggregate amount of revenue reported for the first nine months of 2014 for non-cash transactions was approximately $8,100,000. The reversal of revenue on the non-cash exchange transactions will also impact additional accounts including reductions in Prepaid Assets, Intangible Assets and Amortization Expense. The Company also expects that certain expenses will be reclassified. Additional adjustments may be identified pursuant to the ongoing review and analysis. The Company has also begun a review of calendar year 2013 activity to determine whether there are any adjustment that may impact previously issued financial statements. There are no known adjustments to 2013 financials at this time. The cash balance is not impacted by these changes.”

One would think that after such a major restatement – the restatement reduced $8.8MM in revenues reported for the first 9 months of 2014 by 97% – that AEYE would fire its auditors, MaloneBailey. But it didn’t, and MaloneBailey continues as AEYE’s auditor – and, we believe, that this is a red flag which may cast doubt on AEYE’s financials. If MaloneBailey can’t get revenue right – quite literally the top of the P&L and the driver of the business – why was it allowed to remain as the company’s auditor? Worse yet, does their continued presence mean that this previous level of inattention persist today? We are befuddled.

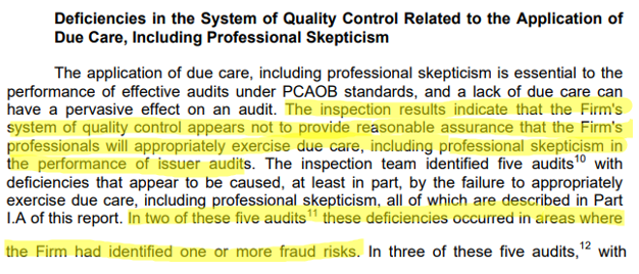

We believe AEYE’s auditor lacks credibility and presents meaningful risk to investors

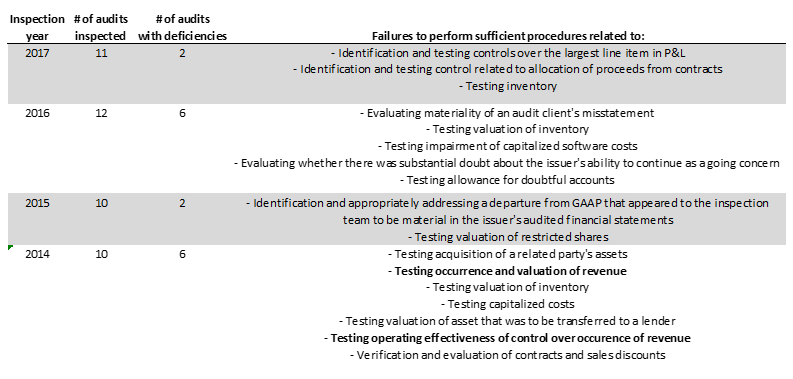

MaloneBailey, it turns out, seems to have a pattern of audit issues – from 2009 to 2017, the PCAOB inspected a total of 97 of MaloneBailey’s audits, and found 33 audits with deficiencies, 34% of the sample. We present findings from the last four inspections below – we believe that this commentary shows a pattern of simply accepting whatever company management teams present MaloneBailey as their financials:

The 2014 inspection commentary is particularly striking:

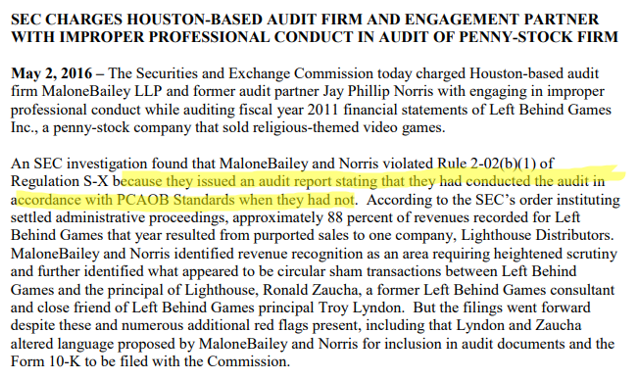

It should perhaps come as no surprise that the SEC charged MaloneBailey’s and one of its audit partners with improper professional conduct in connection with its audit of Left Behind Games. Just the year before, the audit client referred to in the charges, Left Behind Games, had its executive Ronald Zaucha fined $2.6M by the SEC and was permanently banned from trading stocks. The charges imply that Zaucha and Lydon altered language proposed by MaloneBailey.

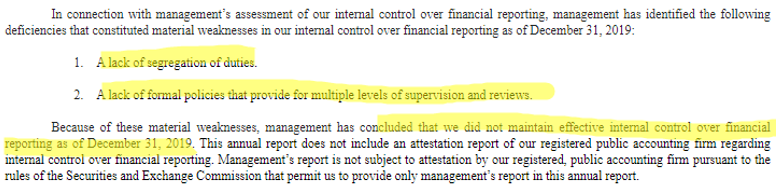

This is made worse by the fact that AEYE continues to have a material weakness in internal controls over financial reporting:

Changes to historical accounts

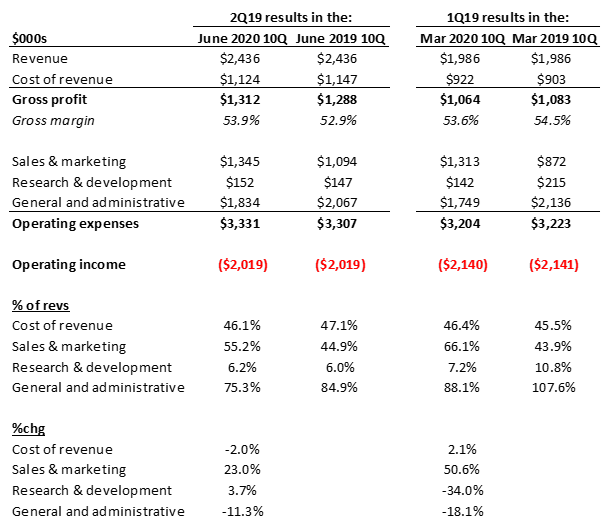

We believe that AEYE’s combination of a material weakness in internal controls over financial reporting and its auditor’s numerous negative regulatory comments and SEC charges should not inspire confidence in investors. In fact, we found changes their most recent quarterly results that should be cause for concern – it appears that AEYE’s management has reallocated costs (“reclassified” and “amended the categorization of”, in their words) in its historical financials in a manner that could make them look “better” in the eyes of investors.

In both the June 2020 and March 2020 10-Qs, the prior period (June 2019 and March 2019) quarterly income statements have had costs reallocated:

While there has been no change in operating income:

- It appears that costs of revenue were shifted (and moved from opex) from June 2019 to March 2019, making the sequential gross margin transition from March to June go up 30bps versus going down 160bps, creating a more stable gross margin trend

- Operating expenses also changed, with dollars being reallocated from G&A to sales & marketing – this, in our view, also “dresses up” the financials – investors are much more likely to look favorably on a business that is spending more on sales & marketing than G&A

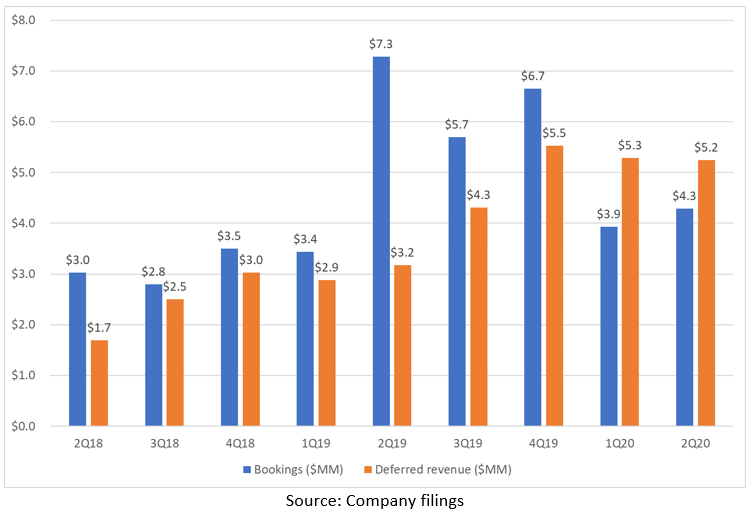

Deferred revenue growth is nonexistent in 2020

In the face of improving metrics and revenue growth, one would expect to see growth in key SaaS metrics. Typically, for SaaS businesses, growing deferred revenues and bookings are a sign of continued customer adoption and future revenue growth, which is why SaaS businesses command high valuation multiples. After a large one-time customer win in 2Q19, which was reflected in AEYE’s bookings (and the reason why 2Q20 bookings were down 41%), bookings have steadily fallen, and deferred revenue is down 5% from YE19:

Contrast this to MSFT, for example, which is a giant company whose growth should be constrained by its size – MSFT’s June deferred revenue balance is up 26% in the first six months of 2020. One would think a smaller, more nimble company like AEYE in an allegedly attractive space would be able to beat that.

The Mariner Instant Replay:

- AEYE has previously had to restate its financials due to issues related to revenue recognition

- AEYE’s auditors, MaloneBailey, displays a pattern of failing to obtain sufficient evidence for its audit opinions and has been charged by the SEC

- AEYE currently has a material weakness in its internal controls over financial reporting

- AEYE has recast its historical expenses

- AEYE’s stalled out deferred revenues may be a signal that growth is not as sustainable as reported

All this begs the questions:

- Can shareholders really trust AEYE financial statements or auditors after such material restatements and questionable activity in its accounting practices?

- If the company’s financial metrics improve over the next few quarters, is such an improvement believable? In our opinion, AEYE’s accounting practices and auditors create an unquantifiable risk for shareholders

Even if we were to believe the company can fix its management and accounting slip-ups, the company’s core product is at best uncompetitive, in our view.

- Finally, can shareholders trust management (and a board) with questionable histories who decide to double down on auditors who can’t catch basic restatements?

- If they keep them around, are they hiding something we are missing?

Conclusion & valuation: reasons to steer clear

Given our concerns about management credibility, a seemingly undecided product strategy, low relative R&D spend, what appears to be a weak, if not captured, auditor, a material weakness in internal controls, and historical accounting changes, we believe AEYE presents significant risks to investors.

We believe that the stock’s ~585% move from March to now is largely unjustified, and has to with investor perception about AEYE’s growth.

After scoring a large one-time deal in 2Q19 that grew bookings 140% year over year, bookings in 2Q20 have normalized down 41% to approximately $4.3MM a year. This places the company at a bookings run rate of just 25% above where it was running in 1Q19, making the 38% revenue growth estimates for 2021 likely unattainable.

We believe that, assuming the numbers reported by the company are true, that this performance does not justify an 8.6x FY20 price/sales multiple. MSFT, by contrast, trades at 10.2x FY20 sales. We think that AEYE, given our management concerns and stalling deferred revenue growth should trade at no more than 4x forward sales of $20MM, implying a price target of $8.24, down approximately 50% from the last close.

Mariner’s Final Word: Remember Your ABCs (Always Be Cautious)

Well done. Everything the Kerr/Quiel clans touch is garbage. Past is prologue and pedigree counts.

https://buyersstrike.wordpress.com/2012/05/02/humble-harold-sciotto-sefe-ecty-augt-spdl/