Portfolio manager summary

GreenPower Motor (TSX: GPV, NASDAQ: GP) is an EV bus company that we believe has significant misunderstood risks:

- Unlike certain EV plays (cough, cough, NKLA), GreenPower actually has revenues! The problem is that those revenues are entirely from California, and have been dependent on a subsidy program that we estimate accounted for ~74% of calendar year 2019 and 2020 YTD revenues

- As a result of state budget constraints, the subsidy program itself is expected to keep shrinking – we believe this dynamic has already started to affect GreenPower’s revenues, which are down 41% compared to the same period in the prior year

- We believe that GreenPower has prioritized G&A over R&D, having spent ~$2MM on R&D over the last five fiscal years while spending close to $8MM on “Administrative Fees”; this is perhaps the reason why GreenPower has no patents and licenses, and could explain the inconsistencies we found in how the company has marketed its products in press releases compared to how it discloses the specs on its vehicles

- We believe that CEO Fraser Atkinson has kept some questionable people in his orbit of colleagues – his prior endeavors have seen SEC subpoenas, a delisting by the BC Securities Commission, and collapsing stock prices

- One of GreenPower’s major shareholders is a BC bus entrepreneur who owned a company implicated in deaths of two teenagers in a crash that was determined to be due to a “flagrant disregard for safety provisions”

- Another (former) major holder of GreenPower is reputed by penny stock investors as having a history of “toxic financings”. They were also a holder of SCWorx, a company recently halted by the SEC

- The PCAOB imposed sanctions on GreenPower’s auditor, Crowe MacKay, related to a 2014/2015 audit, and the PCAOB noted deficiencies related to a 2017 audit that included “the inappropriate issuance of an audit report without having planned and performed an audit under PCAOB standards”

- We believe that GreenPower’s revenue growth is likely to be significantly hampered due to the shrinking California subsidy program – this, compounded with the governance risks outlined above, leads us to assign a $2 price target to GreenPower’s stock, down 84% from the last close

Despite having real revenues, GreenPower has major risks misunderstood by retail investors

GreenPower Motor Company (TSX: GPV, NASDAQ: GP) is a British Columbia-based designer, builder, and distributor of all-electric buses used in various applications. It is the product of a 2014 reverse merger into Oakmont Minerals, which at the time was being run by current GreenPower CEO Fraser Atkinson.

GreenPower’s product offering is comprised of:

GreenPower EV Star Min-E – Which is an electric mini-bus available in four configurations and with a “life expectancy of ten years”

The Beast– A Type-D School Bus which is offered in two different lengths and configurations

EV Transit Bus Line– GreenPower’s low-floor transit line that features multiple models: 30-ft EV250, 40-EV350 and the double decker EV550

With all the hype about EVs out there, and a great many charlatans pumping their technologies, the combination of EV and reverse merger might leave a skeptical investor questioning this company.

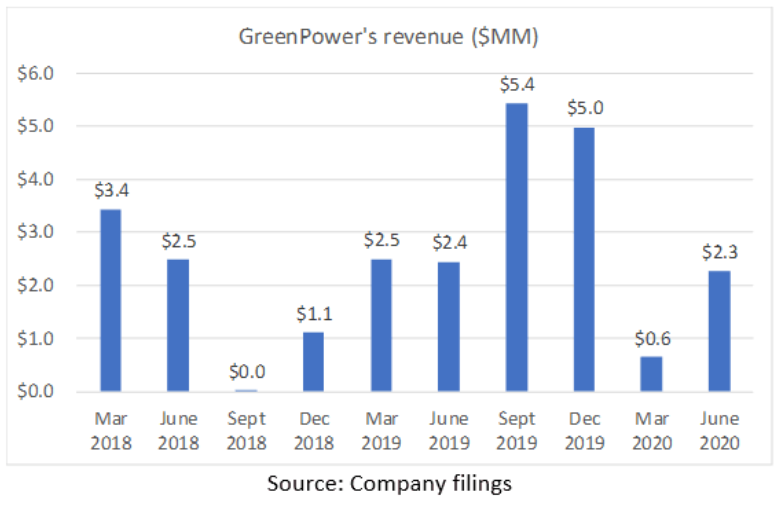

Much to our surprise, and, we would imagine, to yours, GreenPower has achieved the first step to establishing a real business and has booked approximately $25.3MM in revenue since March 2018, which on the surface, seems impressive, but we believe is unlikely to be sustainable.

GreenPower’s stock is up ~767% this year and up ~300% since July – before we delve into why we believe this is unjustified, let’s recap the long case:

- GreenPower has revenue! More than what NKLA can claim – which gives GreenPower real legitimacy as an EV business

- A hype-driven exponential increase in investor interest in the EV space and trade opportunities created because of the rise of EV stocks such as TSLA (up ~410% YTD) and NKLA (up ~167% YTD)

- Electric buses are a unique segment of the EV market, not pursued by many public companies (perhaps the closest public competitor is Ballard Power)

- Increased government investment in the EV infrastructure, especially electric buses

Mariner Reality Check: The wheels on the bus are slowing down

We believe GreenPower’s revenue is about to fall off a cliff as a result of its exposure to California’s subsidy program. GreenPower is only registered as a motor vehicle manufacturer and dealer in California, and the company has “not yet sought formal clarification of our ability to manufacture or sell our vehicles in any other states.” In our view, this effectively makes GreenPower a “one-state” wonder.

We believe that revenues to date have been supported significantly by one government program (we estimate that 74% of GreenPower’s total revenue in calendar years 2019 and 2020 YTD is from the program): California’s Hybrid and Zero-Emission Truck and Bus Voucher Inventive Project (HVIP).

Funds allocated to HVIP were fully claimed by November 2019, no new funds have been allocated, and HVIP expects the next allocation to be lower – thus far, we have seen GreenPower’s YTD 2020 revenues fall 41% from the same period in 2019 – we expect them to fall further given shrinking HVIP program funding.

Like the bus in Speed, we believe the shrinking HVIP program is the proverbial bomb in the bus, as EV truck/bus producers fight for a piece of a smaller pie – except Sandra Bullock isn’t there to steer the bus to safety and Keanu Reeves isn’t there to defuse the bomb.

In this report, we explore the risk of falling HVIP credits, GreenPower’s claims about its products and autonomous driving, the CEO’s history with seemingly questionable characters (hint: SEC allegations) and an auditor with PCAOB deficiencies.

The combination of all these factors leads us to believe that GreenPower’s stock, trading at 16x 2021 revenues, is inappropriately valued, and assign a price target of $2, down 84% from the last close.

We believe that a shrinking HVIP credit program poses the number one risk to GreenPower’s topline and its future growth

At first blush, electric vehicles are extremely expensive compared to their ICE counterparts. An average diesel transit bus costs $500,000, compared to an EV bus at $750,000, while a diesel school bus costs around $110,000 compared to an EV school bus at $230,000.

Because of this pricing differential, governments have long offered subsidies to bring the cost of the vehicles close to their cheaper, gas-powered peers and induce usage of cleaner technologies to mitigate harm to the environment.

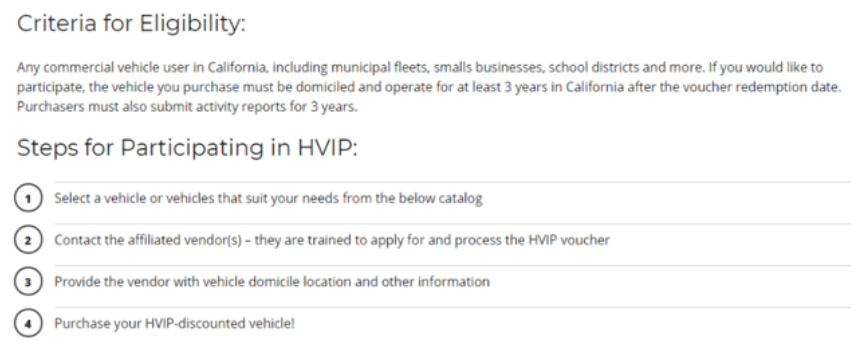

Since GreenPower is only registered as a motor vehicle dealer in California, the ONLY truly relevant subsidy program in our view is California’s Hybrid and Zero-Emission Truck and Bus Voucher Inventive Project (HVIP). The HVIP program was established in California following the passage of the California Alternative and Renewable Fuel Carbon Reduction Act and to date, HVIP has deployed more than 4,000 medium-to-heavy duty vehicles across 1,100 participating fleets.

The California HVIP works as follows:

- Every budget year, the California Air Resources Board (CARB) sets a budget that will be allocated to the HVIP program

- Vehicle buyers submit purchase orders to dealers, and the dealer uses that order to apply for the HVIP voucher

- The purchaser will receive the vehicle at a discounted price at point of sale, while the dealer will receive the incentive payment from HVIP as well

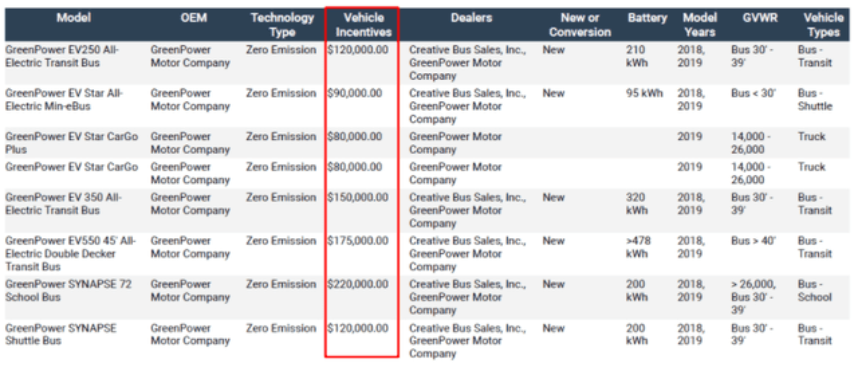

In the case of GreenPower, HVIP provides the following incentives for its products:

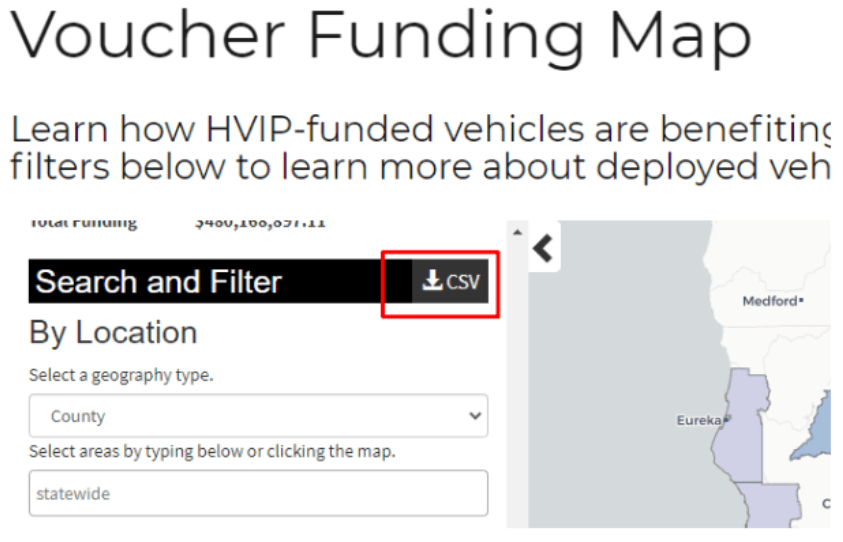

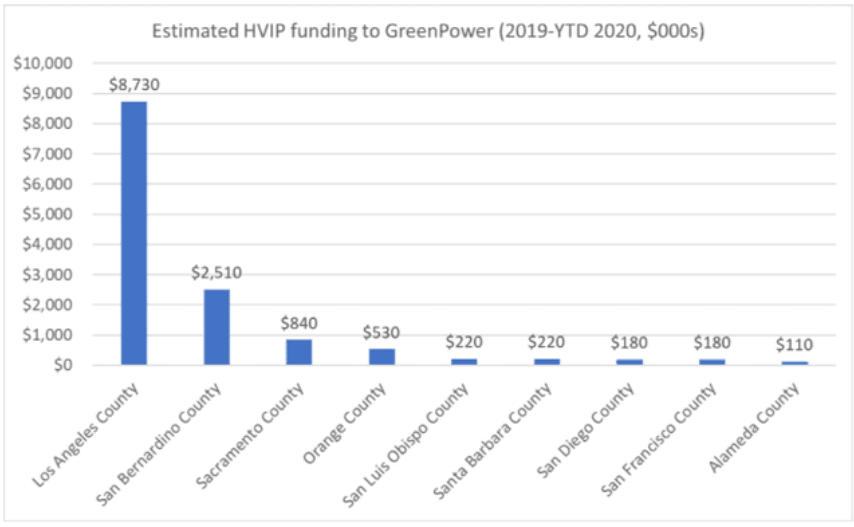

These incentives allow for an effective reduction in the price of the vehicle for the end user, and have been a meaningful source of revenues for GreenPower. The Voucher Funding Map allows users to download a CSV file to show how much funding GreenPower has gotten from the HVIP program:

The data set shows GreenPower received approximately $13.5MM in funding from HVIP for what we believe to be calendar 2019 and YTD 2020 (since GreenPower only began mentioning the program starting in 2019). Over this same period, GreenPower has reported $18.3MM in revenues – this implies that HVIP has been responsible for 74% of GreenPower’s revenue for calendar years 2019 and YTD 2020, making it a very important source of revenue.

Why does this matter? If ~3/4ths of GreenPower’s revenues are associated with one state subsidy program and the budgetary authority is reducing their funding, that creates quite the pickle for GreenPower; not to mention that demand for these vouchers has been increasing.

- We called HVIP, and learned that by May 2019, funds allocated for the HVIP voucher program for the July 1, 2018 to June 30, 2019 fiscal year had already been claimed, so a waitlist for the next fiscal year’s allocation was started

- According to GreenPower, on October 24, 2019, CARB approved funding of $142MM for the fiscal year starting July 1, 2019 until June 30, 2020 – because there was a $125MM waitlist already extant, the entire $142MM was spoken for by November 2019 – it follows, in our view, that funds for any GreenPower order that arrived after November 2019 are simply not available

- Unlike prior years, HVIP did not start a new waitlist, and will not be announcing new funding until early 2021

- The implication, in our view, is that new HVIP subsidy funding for GreenPower has been effectively unavailable since November 2019, and will, best case, be available in early 2021 – this represents over a year without incremental subsidy funding to help drive demand for GreenPower’s orders

- The HVIP representative told us that they expect the next funding round to be less than the $142MM in funds for the 2019-2020 period. This would make sense given California’s spiraling budget deficit – in January 2020, the state was projecting a $5.6B surplus,which has now turned into a $54B deficit on plummeting tax revenues

This dynamic seems to be hitting GreenPower already, as June 2020 YTD revenues are down 41% versus the same period in 2019.

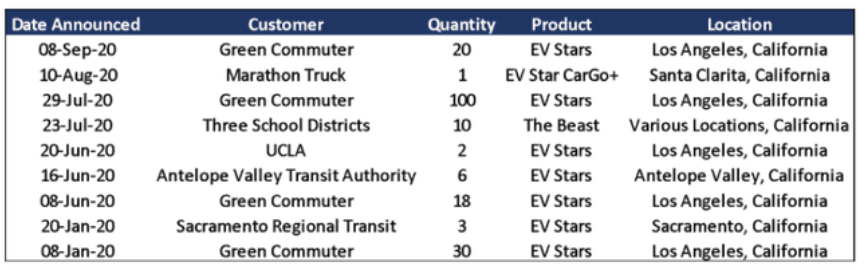

Based off the press releases from the company, above are the orders/deployments announced by GreenPower since the beginning of the year. On top of most of these orders being announced since June (after the stock caught fire and almost 8 months since funding closed), the startling fact is that all these orders are from California based customers, suggesting their dependence on HVIP funds.

We view HVIP as a key demand driver for buyers of EV buses – without subsidization, we believe that few municipalities or customers have the wherewithal to purchase premium priced EV vehicles. This, combined with the fact that HVIP has been such a meaningful contributor to GreenPower’s revenues and concentration of orders in California, leads us to believe that GreenPower’s revenue growth is about to be seriously hampered as the HVIP program shrinks. If these customers do not receive HVIP funding, will they really follow through with these orders?

The Company has shied away from talking much about subsidies and their significance as a potential headwind; however buried in its filings, GreenPower itself has also mentioned the negative impact of HVIP funding:

“On November 1, 2019, CARB announced that it had received voucher requests for the entire $142 million budget allocated to the HVIP program for the current fiscal year and was no longer accepting new voucher requests until new funding for the program is identified. This announcement has negatively impacted new sales prospects for GreenPower buses in the state of California and any further reduction or elimination of the grants or incentives in the state of California would have a material negative impact on our business, financial condition, operating results and prospects.”

For the quarter ending December 2019:

“by November 1, 2019, CARB announced that it had received voucher requests for the entire budget allocated to the HVIP program for the current fiscal year and was no longer accepting new voucher requests until new funding for the program is identified. This announcement has negatively impacted new sales prospects for GreenPower buses in the state of California.”

We believe the market underappreciates the risk that is posed by the HVIP program:

- While the program has led to revenues for GreenPower in the past, it has made the company almost entirely dependent on the HVIP and California ecosystem

- Given our estimate that ~3/4 of the company’s revenues are from the HVIP program and all the announced orders since January originating in California, we believe that the shrinkage of the HVIP and its increased competitiveness poses a huge risk to the company’s topline

- This has already started to impact the company in our opinion, with YTD revenues down 41% compared to the same period last year, but we fear the worst is yet to come

Not only are the state subsidies trouble for GreenPower, we believe that the company’s R&D and product marketing are a cause for concern.

Product marketing and R&D concern us…a lot

The EV industry is still very much at a nascent stage and companies within the industry need to be constantly innovative to stay on the forefront. Some of the most adopted EV products available today, i.e Tesla products, are the product of billions in R&D and product development costs.

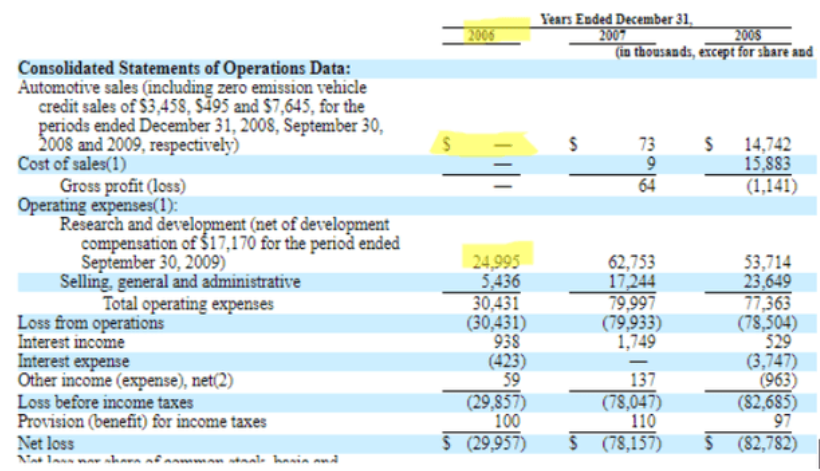

Over the past five fiscal years, GreenPower has spent just $2.2MM on product development – a relatively small dollar expenditure when you consider that TSLA, in 2006, before it had ANY revenue to speak of, spent $25MM on R&D:

To put this in context, TSLA, in a year when it had zero revenues and was still very much a nascent business, spent over 10x what GreenPower has spent in the last five fiscal years.

What GreenPower has spent on is “Administrative Fees”, a cumulative ~$8MM over the same period, or almost 3.6x its product development spend. In our view, we do not believe that companies that claim to be innovative yet spend minimally on said innovations are good investments.

Why spend so much on “Administrative Fees” rather than pursue innovation, as Greenpower lacks substantive IP? “We do not currently have patents and licenses, but may choose to obtain patents and licenses on our designs, processes or inventions in the future.”

Why allocate funds to “Administrative Fees” when those funds could be used to legally protect its own designs and inventions?

We wonder if this lack of spend on product development is the reason for the inconsistencies we’ve discovered in some of GreenPower’s marketing and specifications. GreenPower’s media outreach appears to present outcomes that are much higher than the specifications outlined on its website.

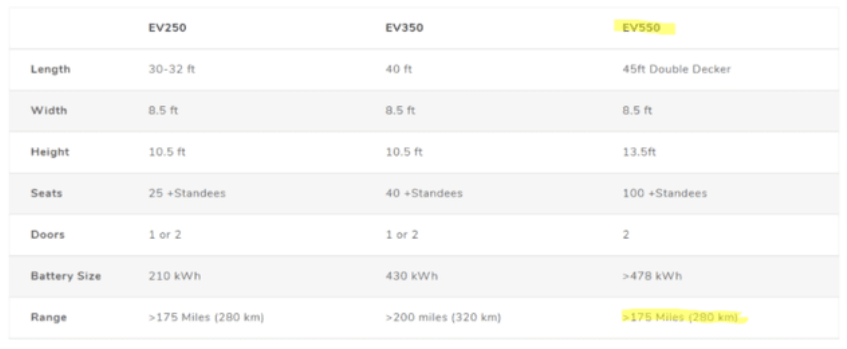

Instance 1: EV550’s range

- In 2016, GreenPower delivered an EV550 bus to the Greater Victoria Harbour Authority – the article covering the delivery noted that the “Last October, GreenPower supplied the Greater Victoria Harbour Authority with North America’s first fully electric double-decker bus. It was also the company’s first delivery, an ‘EV550’ that can travel up to 300 miles on a single charge (MPC)”

- But on GreenPower’s own product site, the EV550 today is characterized by a minimum range of 175 miles

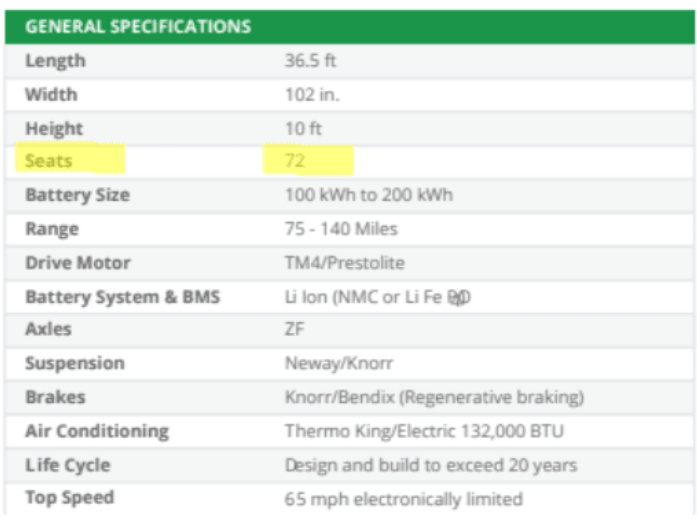

Instance 2: A wide range of seating capacity on the Synapse Shuttle

- In a 2018 letter to shareholders, GreenPower introduced the Synapse Shuttle, which, at the time, allegedly had 72 seats

- But when it delivered the Synapse Shuttle to a client in 2019, the vehicle capacity appears to have shrunk – “The Synapse Shuttle is a thirty-six foot purpose built all-electric bus with seating for over 40 passengers and a range of up to 150 miles on a single charge. The Synapse Shuttle can be configured with multiple charging options including Level 2 on-board charging or Level 3 DC fast charging”

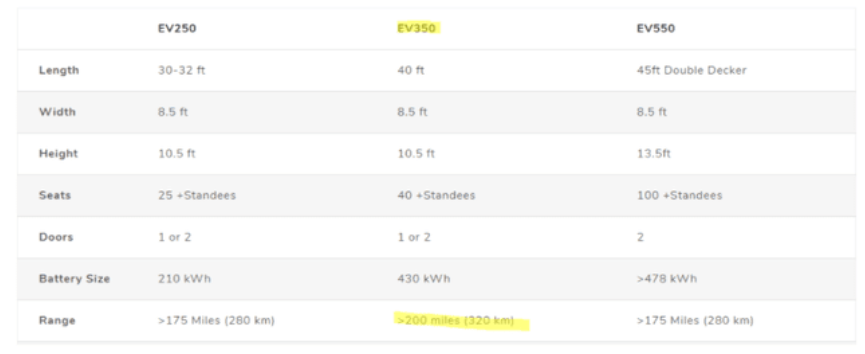

Instance 3: Range estimates for the EV 350

- In April 2018, GreenPower announced that “its EV350 40-Foot All-Electric Transit Bus has outperformed its original range expectations. The zero-emission vehicle recently traveled 205 miles with 50% SOC (state of charge) remaining battery power after the trip” (this implies a 410 mile range in our view)

- But again, on its own product page, GreenPower conservatively presents only the minimum range of the EV350 as 200 miles

These inconsistencies make us question the credibility of GreenPower’s management team – our questions only increase with the announcement that it was developing a fully autonomous vehicle.

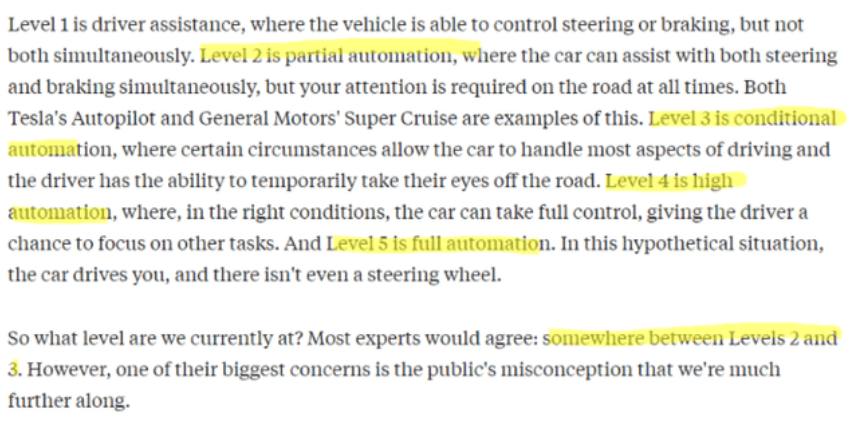

Autonomous driving, like EVs, has been used by to excite and entice investors curious about the future of transportation. During the quarter ending March 2020, GreenPower announced that it had entered into an agreement with Perrone Robotics (“Perrone”) to build a fully autonomous EV Star for the transit market. We are very skeptical that this is anything but hype – fully autonomous driving is notoriously hard and we believe it is unrealistic that this milestone will be achieved in the near future (from Business Insider):

What GreenPower seems to propose is Level 5 automation, which is “decades away”:

GreenPower ’s partner in this effort, Perrone – did a Series A with Intel in 2016 – by the time Perrone received this funding, Google had already spent $1.1B on its autonomous driving project. In 2019, Uber raised $1B JUST for its driverless cars business. We cannot comprehend how GreenPower and Perrone will be able to compete or innovate in this market given the level of capitalization required to invest and subsequently commercialize the technology.

Recall that GreenPower, in the last five fiscal years, has spent just ~$2.2MM in product development while it has spent $8MM on “Administrative Fees”. The company does not have patents or licenses – this causes us to question the company’s autonomous driving claims and goals. How is GreenPower supposed to compete or innovate without protected IP?

We believe that GreenPower should focus on aligning its specifications with its marketing, rather than marketing optimistic cases and instead presenting “minimum” specs. To us, this is not the sign of growing, innovative company.

We believe that the people in the GreenPower ecosystem have serious credibility issues

We are big believers that the people behind a company – the executives, directors, and major shareholders – are critical to the success or failure of the company and its strategy. Their prior business performance, personal conduct, and relationships should be an indicator of the likelihood of success of their current venture, especially in light of the nascent nature of the EV space.

When we evaluated GreenPower’s key personnel, we found what can best be described as a series of red flags – collapsing stock prices, an SEC subpoena, and major shareholders with issues that made us uncomfortable.

Enter Management: Not so “Versatile” after all

In February 2003, GreenPower’s current CEO, Fraser Atkinson, after leaving his position at KPMG, was appointed CFO of a Canadian company known as Versatile Mobile Systems, which traded on the TSX Venture Exchange under the ticker VV. Notably, another Versatile AND GreenPower board member, Malcolm Clay, was also a KPMG alum. At the time, VV was “primarily engaged in software development and sales of computer software, hardware and systems integration services related to wired and wireless mobile business solutions.”

In 2008, VV appointed one Alessandro Benedetti to its board – an Italian gentleman who had, in the early 1990s, been arrested “on charges which included false accounting”, and “entered into a plea bargain with the prosecuting authorities under which he entered a guilty plea and accepted a sentence of imprisonment.”

This doesn’t seem like someone you’d want on your board, right? It seems that Mr. Benedetti has continued to court controversy, having recently been identified by the WSJ as having worked in concert with Softbank’s Rajeev Misra to strike “at two of [Rajeev’s] main rivals inside SoftBank with a dark-arts campaign of personal sabotage”.

In 2009, shortly after Benedetti’s appointment, VV started a private equity subsidiary, Mobiquity Investments Limited, on the fact that the “core strength of our Board of Directors, in particular Alessandro Benedetti and Bertrand Des Pallieres, is in banking and private equity activities.”

Come October 2009, and we find that VV has taken an 8.3% in the Equus Total Return Fund (NYSE: EQS), a Houston-based business development company (BDC) making investments in the debt and equity securities of companies with an enterprise value of between $5MM and $75MM.

By January 2010, EQS’s stock price had fallen approximately 55%, and the VV players (CEO John Hardy, CFO Fraser Atkinson, and the aforementioned Des Pallieres and Benedetti) approached EQS’s existing board asking for board representation. On April 13, 2010, EQS filed a definitive proxy with the SEC to, among other things, consider the election the VV directors.

Just 13 days later, on April 26, 2010, the SEC “subpoenaed records of the Fund in connection with certain trades in the Fund’s shares by SPQR Capital LLP, SAE Capital Ltd., Versatile Systems Inc., Mobiquity Investments Limited, and anyone associated with those entities.”

These entities were all related to one another:

- Mobiquity was a subsidiary of Versatility

- Versatility board members Benedetti and Des Pallieres controlled SPQR and SAE, respectively

We cannot speculate as to what this was related to or amounted to, but we believe it’s fair to say that drawing the attention of the SEC is never a good sign. A letter sent to EQS shareholders on May 3, 2010, characterized the SEC matter as follows: “the Securities and Exchange Commission issued a subpoena and notice that it was conducting an investigation into possible violations of federal securities laws in connection with trading in Equus stock.”

By June 2010, the VV group had been elected to the board on their promises to change the poor governance of EQS, with Hardy winning the Executive Chairman seat and Fraser becoming the Chairman of the Audit Committee. But it seems like they did not live up to their promises, being called to task by a shareholder for:

- “Accounting inconsistencies” – remember that Fraser was Chairman of the Audit Committee!

- “Ridiculous” board salaries, with John Hardy earning “2% of the fund’s current market cap annually”

- “Within 6 months they announced plans for a massively dilutive rights offering”

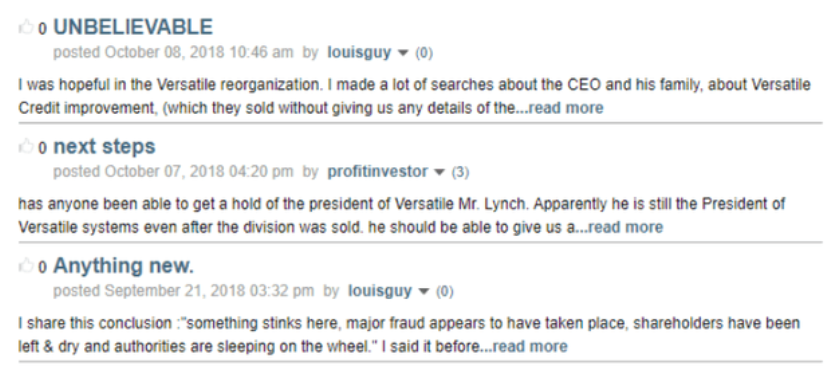

Sure enough, it doesn’t look like Fraser and his crew generated much value at EQS – since being appointed to the board, EQS is down 50%.Versatile itself has suffered a similar fate – by March 2016, it had accumulated a working capital deficit of CAD $3.3MM, accumulated losses of CAD $63.7MM, and “material uncertainty that may cast significant doubt as to the ability of the Company to continue operating as a going concern”.

By January 2017, Versatile received a cease trade order from the British Columbia Securities Commission for failing to file its financials, and was subsequently delisted. Shareholders were caught unaware:

From its peak in 2011 until it was delisted, Versatile fell 14c to 3c, approximately 79%:

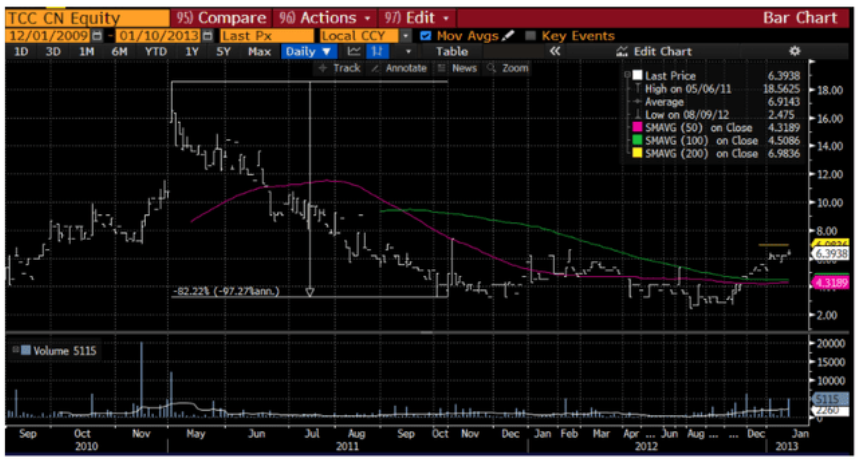

From 2009 to 2013, Fraser was also the Chairman at Rara Terra Minerals, a Canadian mining outfit that trumpeted developments at one of its rare earth properties in November 2012: they believe that they had found “numerous geophysical anomalies on the Xeno property meritorious of geochemical followup next summer.” Barely two months later in January, Fraser resigned from the board and the Company announced a private placement.

In May 2013, Rara Terra later abandoned rare earth mining, and rebranded itself Echelon Petroleum – in 2017, Echelon became Trenchant Capital Corp (TCC CN).

More importantly, Fraser presided over an 82% plunge in Rara Terra’s stock in 2011:

We believe that Fraser Atkinson’s track record speaks for itself – he has aligned himself with seemingly questionable individuals and several listed entities which he was associated with have virtually collapsed in price. Below, we show that his association with potentially dubious individuals continues today.

The RedDiamond connection conundrum

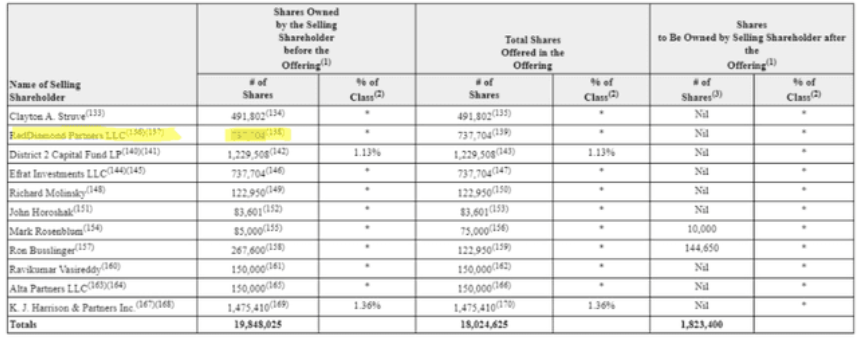

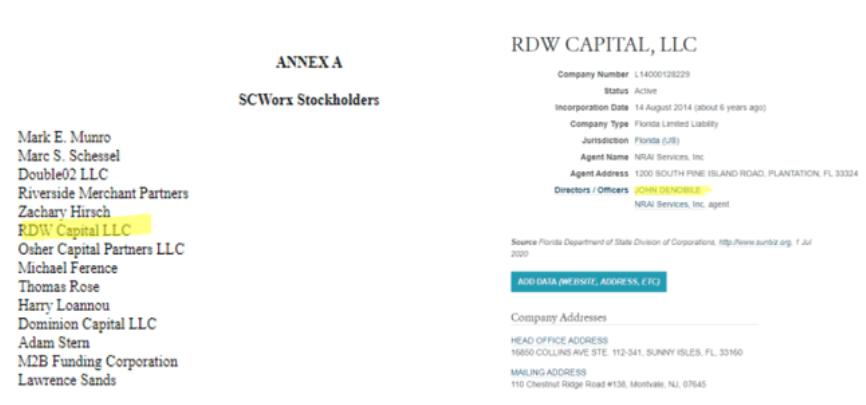

In May 2020, GreenPower released a prospectus to outline the sale of approximately 11.5MM shares by a group of shareholders who obtained their shares through private placements. The selling shareholder table reveals that one of these holders, RedDiamond Partners LLC, was selling all of its 737k shares in the company:

In the footnotes we learn that:

- RedDiamond’s address is 156 West Saddle River Road, Saddle River, NJ 0745

- John DeNobile exercises control over the shares RedDiamond owned

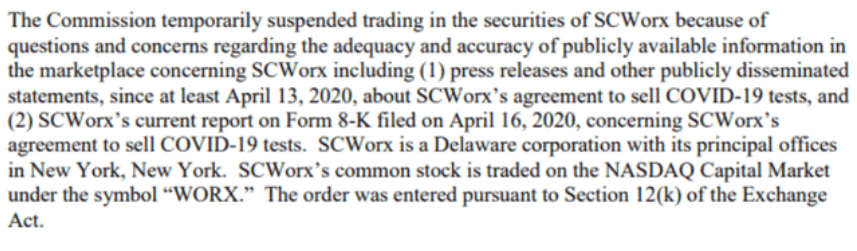

A quick look at RedDiamond’s SEC filings shows that in 2019, RedDiamond held shares in a company called SCWorx, a “provider of data content and services related to the repair, normalization and interoperability of information for healthcare providers and big data analytics for the healthcare industry.”

Yes, that SCWorx (WORX), which was halted for three months by the SEC in April 2020:

SCWorx’s CEO pled guilty to felony tax evasion charges and the Covid-19 test supplier they used had a CEO who was a convicted rapist – huge hat tip to Hindenburg Research for a job well done on this one.

Curiously, while RedDiamond is the DeNobile entity that reported its WORX holding to the SEC, another DeNobile entity, RDW Capital LLC, actually shows up as a stockholder in a share exchange agreement:

DeNobile and his business partners, through RDW and other entities they control, have been criticized by microcap investors as providers of “toxic financing” – a form of discounted financing where the convertible note holder is allowed to convert to equity at a price below market. These shares, since they are issued below market, provide an immediate return to the holder, who can then dump them in the open market, causing the stock price to collapse.

The prior presence of RedDiamond’s shareholder list is yet another apparent indication of the types of people Fraser Atkinson associates himself with, which we believe calls into question his credibility as CEO of GreenPower.

A principal shareholder and a potential “flagrant disregard for safety provisions”

In GreenPower’s US IPO filing, we learn that another principal shareholder of the company is Gerald Conrod:

Imagine if you owned shares in an EV bus company and one of the company’s principal shareholders used to run a bus company that had operations that resulted in death? In our view, this would cause us to be highly skeptical of said EV bus company. This is exactly the situation here.

In 1979, Gerald, along with a partner, started Conmac Stage Lines, after the BC government-owned operator ended tour and charter service. On January 30, 1984, one of Conmac’s buses lost its brakes and crashed, killing two high school students and injuring more than 50 others. A BC coroner’s jury cited a “flagrant disregard for safety provisions” as the primary cause of the crash. “During the 17-day inquest, the jury heard ConMac Stages Ltd. continued to use the 20-year-old bus for high-school trips despite inspections that revealed a cracked frame, poorly anchored seats, a broken speedometer and defects in the braking system.” The jury also heard a former driver say that the “company routinely swapped parts on its buses to meet the standards of motor vehicle branch inspectors.”

Gerald has in fact been involved with Fraser since Oakmont bought Greenpower in 2013, when he held approximately 15% of Greenpower’s shares. We find it hard to imagine why a bus company would want to partner with Gerald.

To recap, GreenPower’s CEO and principal shareholders have seen SEC investigations, significant price declines in the companies they were involved in, and a delisting – we view these are major red flags in the ability of management to execute on the stated vision of the company. We believe this complicates the already precarious situation that we believe exists as a result of the declining HVIP credits.

Given all this, one might hope that GreenPower’s auditors are the adults in the room, but we believe that this is NOT the case. Our findings below, regarding GreenPower’s auditors, further compound our concerns that GreenPower presents unquantifiable risk to investors.

Is GreenPower’s auditor credible?

Crowe MacKay, GreenPower’s auditor, has had its own issues that call into question the reliability and credibility of the company’s financials. In Dec 2018, the PCAOB imposed sanctions and fined Crowe MacKay $25,000:

These sanctions related to Crowe MacKay’s audit of Canadian mining company Hunt Mining Corp.’s 2014 and 2015 financial statements, where Crowe MacKay, among other issues:

- “[F]ailed to exercise due care and professional skepticism, and failed to plan audit procedures to obtain sufficient appropriate audit evidence to provide a reasonable basis for the Firm’s audit report”

- “[F]ailed to consider information in the prior year’s audit working papers obtained from a predecessor auditor”

- Conducted Hunt’s audits under Canadian GAAS instead of PCAOB standards, which was required due to Hunt’s status as a “foreign private issuer for the purposes of United States federal securities laws”

Insanely, Crowe MacKay, a Canadian accounting firm, failed to “evaluate relevant public information” to recognize that its audit client needed to be audited under PCAOB audit standards.

In 2019, the PCAOB released the results of a 2017 inspection which found deficiencies in both the audits that PCAOB inspected:

- For one issuer, the PCAOB found “the inappropriate issuance of an audit report without having planned and performed an audit under PCAOB standards”

- For the other issuer, the PCAOB found a failure to “perform sufficient procedures to test the valuation of a liability”

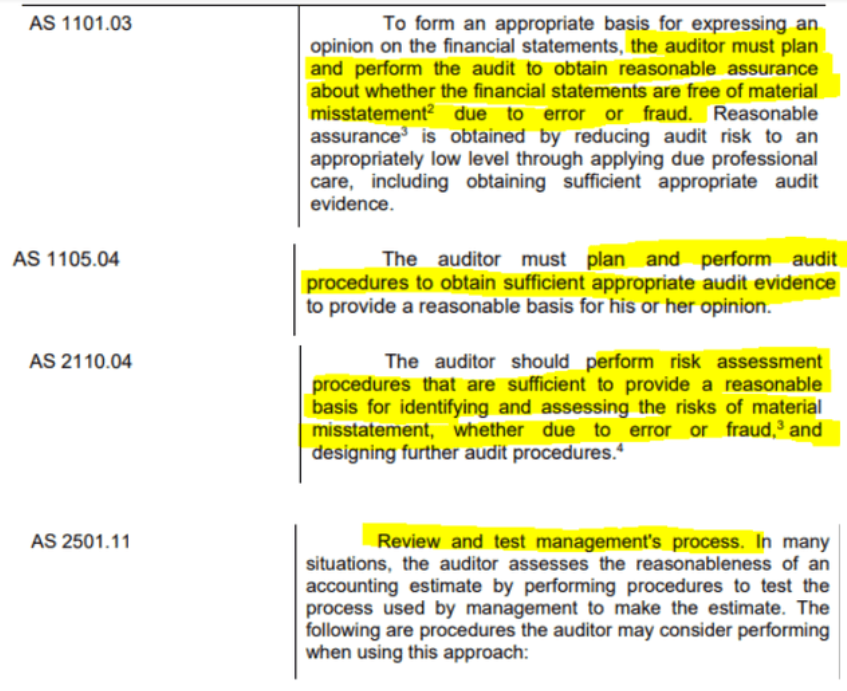

Let’s review that first one – basically, Crowe MacKay issued an audit report without conducting the audit using PCAOB standards – some of the standards that the PCAOB referred to are as follows:

It appears that Crowe MacKay’s shortcomings in its audit practices could be a significant risk to GreenPower shareholders, compounding what we view as management’s checkered history. How can GreenPower’s shareholder believe the company’s financials when the very firm in charge of vetting those financials appears to lack the policies and processes to do so?

Conclusion & valuation

The Mariner Instant Replay on GreenPower is as follows:

- We believe that GreenPower’s revenue growth will collapse as the business is materially exposed to California’s shrinking HVIP subsidy program

- We believe that GreenPower lack of R&D spend calls into questions its competitiveness. We believe that GreenPower’s autonomous driving partnership is unlikely to get off the ground given the difficulty and investment requirements to achieve fully autonomous driving

- We believe that the people in the GreenPower ecosystem have past histories that call into question their credibility, including SEC subpoenas and delistings

- We believe that auditor Crowe MacKay’s history suggests that GreenPower has little in the way of substantial auditor oversight, calling into question the reliability of reported numbers

Let’s be generous and assume a 25% reduction to the next HVIP budget – based on this, we model that GreenPower’s revenues could fall another 25% from the $6MM calendar year run rate implied by the first two calendar quarters of 2020, resulting in forward revenues of approximately $4.5MM.

Being generous (again) and applying TSLA’s FY21 price/sales multiple of 8.1x to GreenPower’s revenues, we arrive at a price target of $2, down ~84% from the most recent close and inline with the stock price before its massive run up. Given the hype and volatility typically associated with EV stocks, we believe the path to our target could be volatile.

Mariner’s Final Word: Remember Your ABCs (Always Be Cautious)

NOTE: Aside from confirming that GreenPower holder Gerald Conrod was in fact the bus entrepreneur that owned Conmac, Greenpower did not respond to our other questions.