Portfolio manager summary

- REKR is a provider of automatic license plate recognition (ALPR) technology whose stock fell precipitously over a lack of legislative progress on the company’s Texas ALPR program

- This appears to be the tip of the iceberg – today, we highlight government documentation which shows that REKR’s revenue opportunities are likely a fraction of what investors expect

- Oklahoma government budgets imply that REKR’s much vaunted UVED program is a sub $2MM revenue opportunity – almost 96% less than the >$40MM in revenue intimated by Rekor’s CEO

- The predecessor provider of this technology to Oklahoma ended its relationship with the state saying the program was “not economically feasible” at a per enrollment fee nearly double what REKR receives

- Government filings showing “Rekor’s largest state and local clients” and our searches of other contracts imply annual revenues of just $1.8MM, a far cry from sellside expectations that contemplate $26MM in revenue in 2021 and $53MM in 2022

- We unveiled evidence that REKR is unlikely to win other states – ALPR bills have failed in several states, including NY and FL, which REKR has touted as potential business opportunities

- In Texas, Rekor appears to have missed its window as the ALPR bill is unlikely to make it to the legislative floor before the May 31 session adjournment. As Texas legislature meets every other year, it won’t see the light of day until at least 2023

- We believe REKR’s largest contributor to 2020 revenue will fall 95% in 2021 due to its non-recurring nature

- Governance concerns combined with management turnover and backgrounds should create an additional level of concerns for investors

- Our work suggests that REKR will be unable to reach sellside revenue estimates, and we assign a $3.71 price target to the stock, down ~68% from current levels

REKR’s revenue problem

Rekor (REKR) is a provider of automatic license plate recognition (ALPR) technology which can be applied to toll roads, parking enforcement, and speed limit and red light monitoring, among other things. On May 10th, REKR saw its shares drop almost 30% which was attributed to “speculation that a Texas bill for uninsured vehicle enforcement [using REKR technology] was likely dead”. It is our view that this is just the tip of the iceberg when it comes to REKR. Today, we show investors the following:

- That the Oklahoma uninsured vehicle program’s revenue opportunity appears to ~96% less than what REKR’s CEO has suggested to investors

- Annual revenue from REKR’s “largest” state and local customers is miniscule relative to future topline expectations

- Evidence that would suggest that adoption of similar legislation in other states is unlikely due to privacy concerns – and yes, we think the Texas bill is dead for at least another two years

- That REKR’s largest revenue driver in 2020 will likely be down 95% in 2021

- Management and auditor concerns

As a result of the above and the implications to REKR’s revenue base, we assign a $3.71 price target to REKR stock, down ~68% from current levels.

CEO Berman seems to have set monster revenue expectations for Oklahoma’s UVED Program

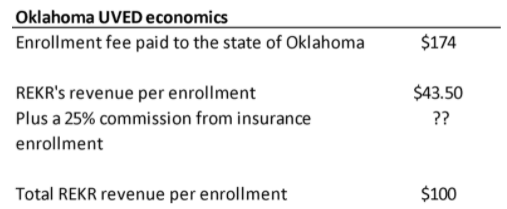

In November of 2020, REKR announced that the state of Oklahoma would use REKR’s Rekor One “to provide vehicle information associated with uninsured motorists as part of the state’s Uninsured Vehicle Enforcement Diversion Program (“UVED Program”)”. The UVED Program uses REKR’s ALPR technology to identify uninsured vehicles, at which point the motorist receives a notice to enter the UVED Program by “acquiring insurance and paying a $174 enrollment fee, thereby avoiding the possibility of criminal charges, associated penalties, and a permanent mark on his or her driving record.”

REKR’s share in this is a $43.50 processing fee per UVED enrollment and a 25% commission from insurance companies for each sign up, bringing the total revenue per enrollment “closer to $100 per successful” enrollment, according to REKR’s CEO, Robert Berman:

Source: Press release, NobleCon virtual presentation

Berman himself outlined the revenue opportunity from the UVED program in an January 2021 virtual presentation at NobleCon (starting around minute 34) – he appears to suggest there are 500,000 uninsured motorists in Oklahoma, with a target to have just 10% of those remain uninsured, implying 450,000 enrollments at close to $100 a pop, for a total three-year revenue opportunity of $45MM, or $15MM annually over the three year life of the contract.

Oklahoma government documents imply revenues ~96% below Berman’s target

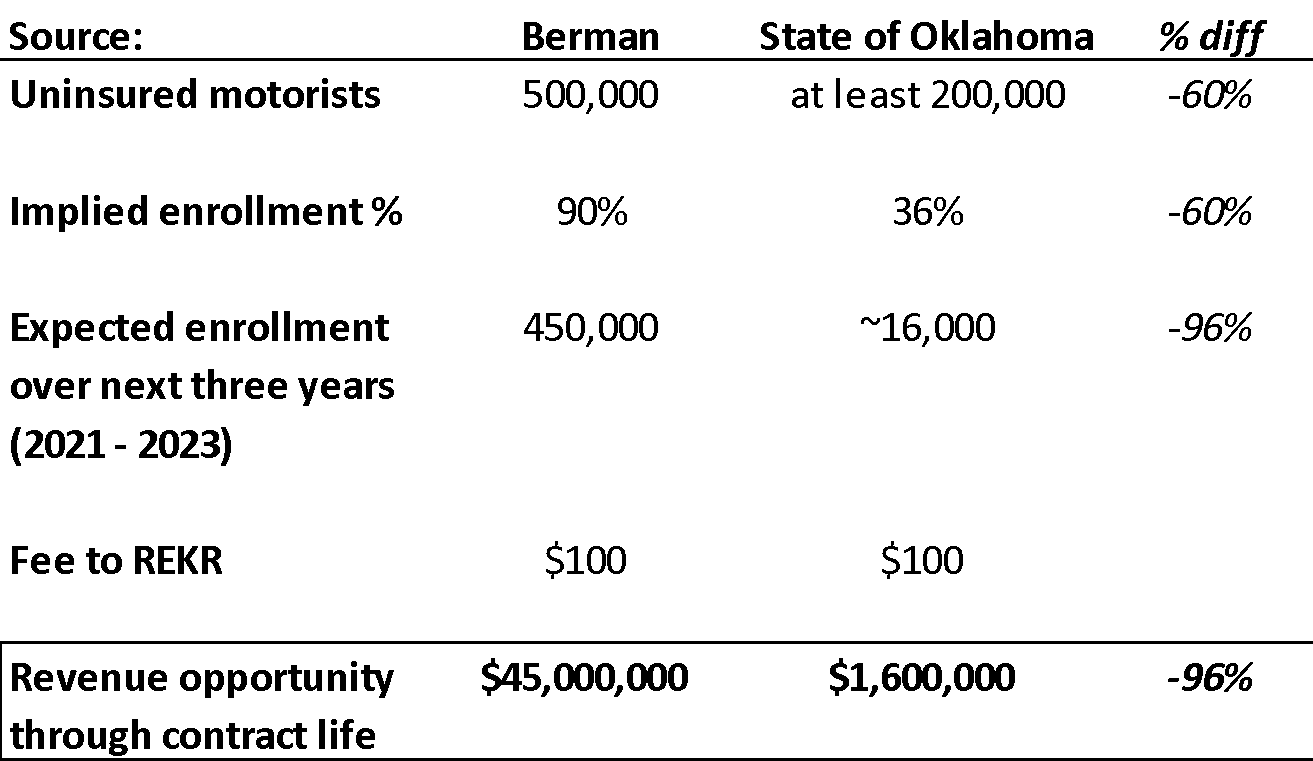

- According to a September 2020 Amendment of Solicitation for the UVED Program, “Oklahoma Insurance Department data indicates at least 200,000 uninsured vehicles exist in Oklahoma”, a far cry (and 60% difference) from Berman’s 500,000

- At year end 2020, the Oklahoma Executive Budget shows 20,678 total enrolled citizens in the program, with an expectation of just under 16,000 more enrollments through 2023:

Source: Oklahoma Executive Budget 2022

- Berman’s 450k enrollments out of 500k uninsured drivers implies an enrollment rate of 90% – the actual enrollment rate for the first six months of 2020 was just 36%

Source: Amendment of Solicitation

What this results in is a dramatically lower revenue opportunity that what Berman intimated during the investor presentation:

It is our view that the Oklahoma revenue opportunity is just 1/28th (1.6MM/45MM) of or 96% lower than what Berman intimated during the investor presentation.

REKR’s first quarter 2021 earnings corroborate our view

REKR reported $245,000 in Oklahoma revenue for itself, and $1,000,000 in revenue for the state of Oklahoma – “over 25,000” notices of non-compliance were issued, but REKR doesn’t disclose the number of enrollments, which drive REKR’s revenue. Based on $174 per enrollment received by the state, this implies an enrollment rate of just 23%, even lower than the 36% rate we mentioned above. For REKR, $245k in revenue divided by 5,747 enrollments implies a revenue per enrollment of $42.63, very close to the $43.50 stated in the contract win and well below the $100 per enrollment fee Berman referred to (this math corroborates our view that REKR’s opportunity is much smaller than advertised and comports with the government documentation above):

Source: REKR 1Q21 earnings

We asked REKR if they could share the number of OK enrollments they got in 1Q21, and what its targeted OK enrollments are – REKR’s EVP Charlie Degliomini responded by asking about our employment and stated that “Much of what you are asking for beyond what is in the Q is material non public information.”

Oklahoma UVED: “not economically feasible” even at higher prices

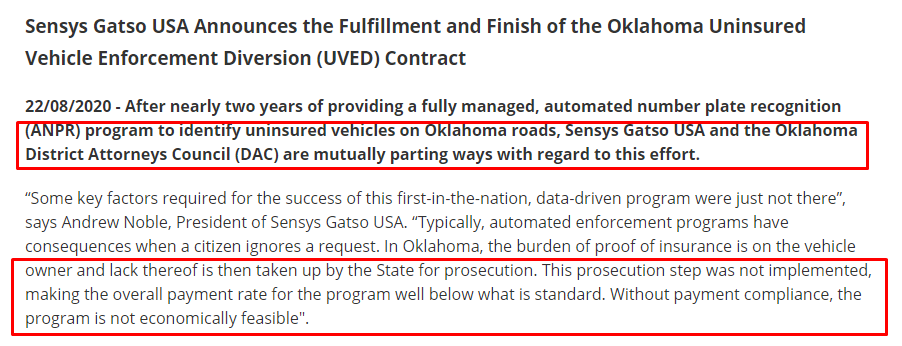

Given these unit economics and trends, it should then come as no surprise that the prior UVED program vendor parted ways with the state, calling it “not economically feasible”.

In its 2017 annual report, Swedish company Sensys Gatso size its Oklahoma UVED contract win at 17 million Swedish Krona, or $2MM annually. Sensys would be paid $80 per enrollment, according to the contract.

Even at a per enrollment fee of near double REKR’s, Sensys, in August 2020, announcing it was “mutually parting ways” with the Oklahoma UVED Program, citing a lack of payment compliance by drivers, making the program “not economically feasible”:

Source: Sensys Gatso release

The sellside has REKR doing $26MM in revenue in 2021 and $53MM in 2022 – the economics of this contract plus the historical precedent suggests this is not remotely possible.

In our next section, we show government documents that suggest that REKR’s largest state and local clients are unlikely to be major sources of revenue.

Public data implies a large gap between actual revenue generation and expectations

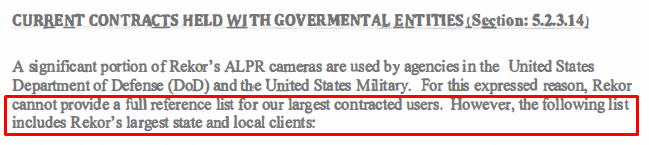

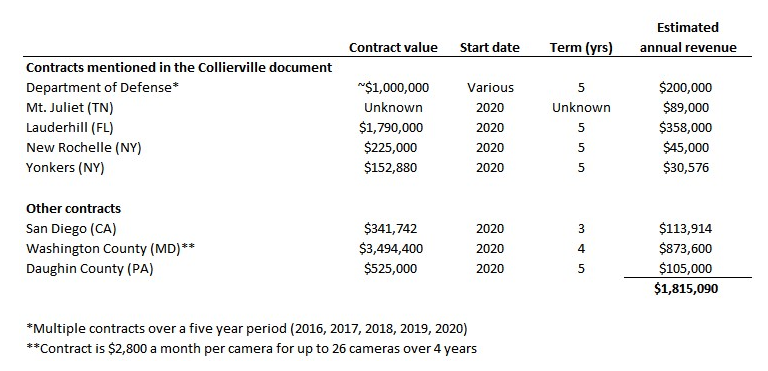

In an October 2020 contract with the town of Collierville, TN, REKR provided a “list [that] includes Rekor’s largest state and local clients”:

Source: Town of Collierville, p60

This list includes the DoD, Sands Point (NY) Real-time Crime Center, Westchester County (NY) Real-time Crime Center, Mt. Juliet (TN) Citywide LPR System, City of Lauderhill, FL, City of New Rochelle, NY, and the City of Yonkers, NY. This got us down the rabbit hole of finding the economics for these contracts and others – what we found were implied annual revenues that make it hard to understand how REKR will hit street estimates. Our view is that if these are the largest state and local clients for REKR, and their revenues are well below $1MM annually, then it is hard to understand how REKR will grow in line with Street expectations.

In the table below, we found contracts for five of the six entities mentioned in the Collierville RFP, as well as three more entities, which total just $1.8MM in annual revenue – and that’s without adjusting for the $1.5MM already likely recognized for the Lauderhill contract (more on this later). Adjusting for this, this set of “Rekor’s largest state and local clients” produces approximately $1.5MM in annual revenue.

Sources: DoD, Mt. Juliet, Lauderhill, New Rochelle, Yonkers, San Diego, Washington County, Daughin County

The contract size issue we raise also extends to the North Dakota win Berman mentioned in the 1Q21 earnings:

Source: 1Q21 earnings call

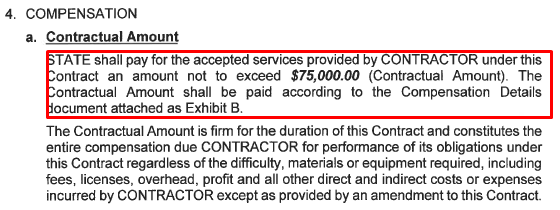

Through public records, we were able to get a look at the contract, and total value of just $75,000 over two years:

Source: North Dakota Parks and Recreation

If “Rekor’s largest state and local clients” produce just $1.8MM in annual revenue, and a recent contract just $37,500 in annual revenue, how is REKR supposed to hit sellside revenue estimates of $26MM in revenue in 2021 and $53MM in 2022??

We asked REKR if they could share detail on their largest client – REKR’s EVP Charlie Degliomini responded by asking about our employment and stated that “Much of what you are asking for beyond what is in the Q is material non public information.”

In our next sections, we show historical evidence that suggests that ALPR bills have little chance of success, and yes – we believe that the Texas bill is dead.

Privacy concerns about UVED programs

In the same investor presentation we mentioned above, CEO Berman cited other states as potential UVED revenue opportunities for REKR. In a 2021 acquisition proposal to Iteris, Berman restated the “large revenue opportunity” of the Oklahoma UVED contract, and told Iteris’s CEO that he expected to “win similar mandates from the States of Texas, New York, and Florida”:

Source: Letter to Iteris

Our view is that UVED programs are unlikely to spread past Oklahoma, which is the only state in the US with an ALPR-powered uninsured motorist program.

This view is rooted in serious privacy concerns associated with reading and scanning license plates:

- An article in the Vermont Law Review argues that the Fourth Amendment extends to license plates, and “that law enforcement officers cannot search a driver’s license plate number without cause”

Recent failures suggest that other states are unlikely to adopt similar programs to Oklahoma

This view seems to have percolated more broadly, as bills to enact ALPR-powered programs appear to have failed across several key states:

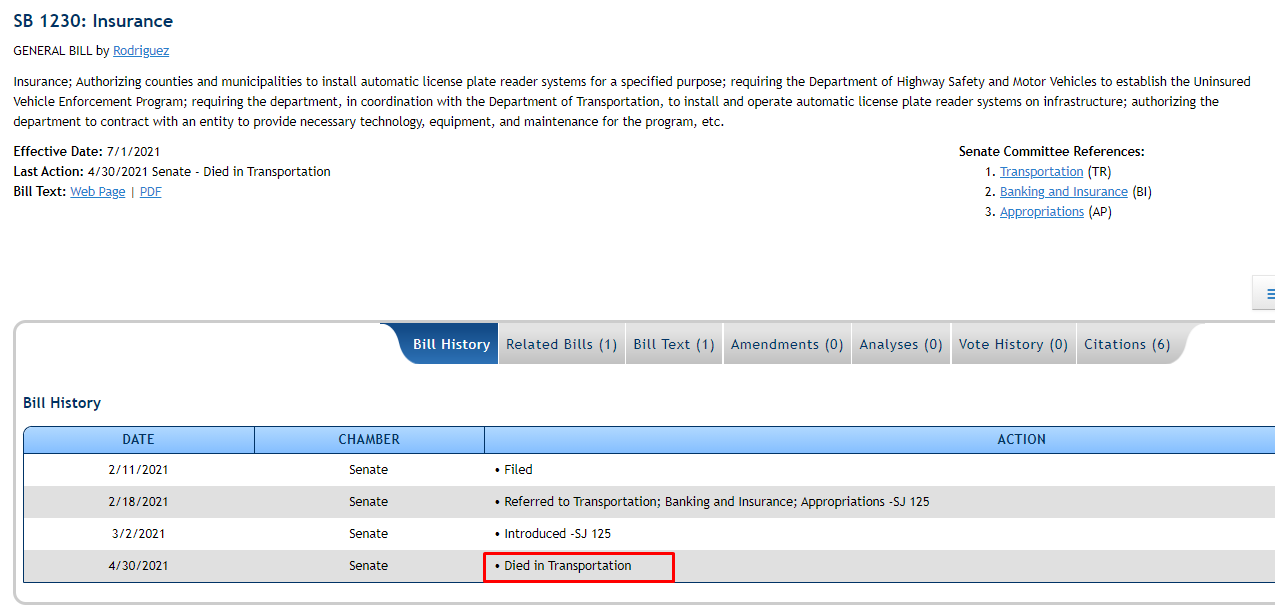

- Florida bill SB1230 died in committee on 4/30/21

“Died in Transportation”

Source: Florida Senate

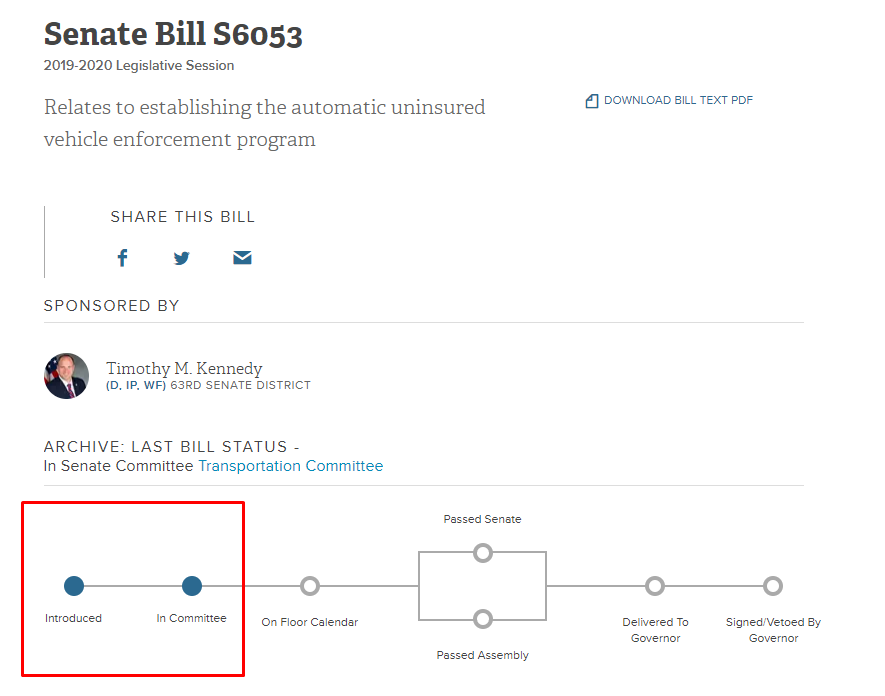

- It appears that New York Senate Bill 6053, which was to establish the “automatic uninsured vehicle enforcement program” never left committee during the 2020 legislative session, and it doesn’t look like there is one for the 2021-2022 session

Source: NY State Senate

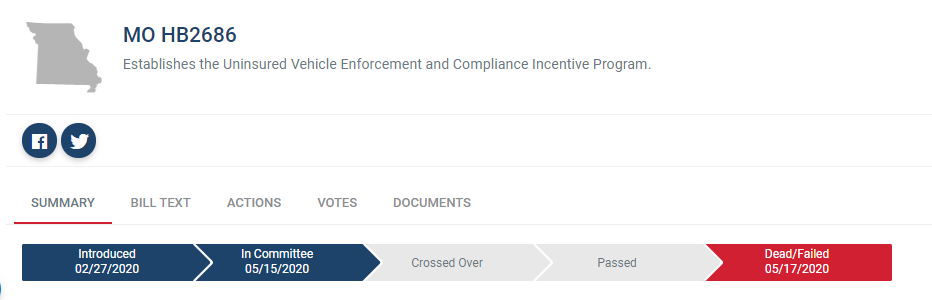

- Missouri’s HB2686, which contemplated using “an automatic license plate reader provider” for uninsured vehicle enforcement, died/failed on 5/17/20

Source: Billtrack

- In 2016, Rhode Island Senate Bill 2231 didn’t make it out of committee, as the “Committee recommended measure be held for further study”

Source: Legiscan

- In 2015, Louisiana governor Bobby Jindal vetoed a similar plan, characterizing the use of ALPRs as making “private information readily available beyond the scope of law enforcement, pose a fundamental risk to personal privacy and create large pools of information belonging to law abiding citizens that unfortunately can be extremely vulnerable to theft or misuse”

The Texas bill: looking deader than a run-over armadillo

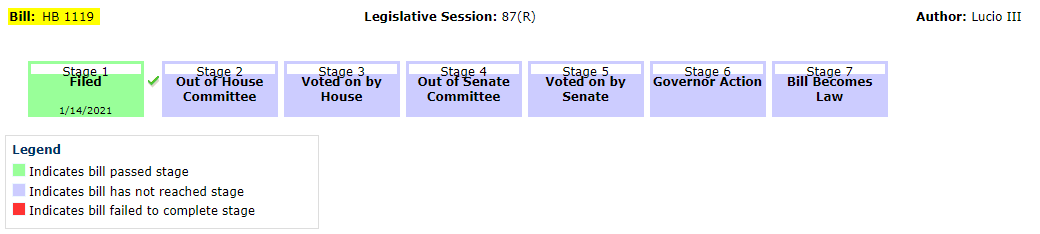

Our research shows that the bill was left pending in committee as of 4/15/21:

Source: Texas Legislature Online

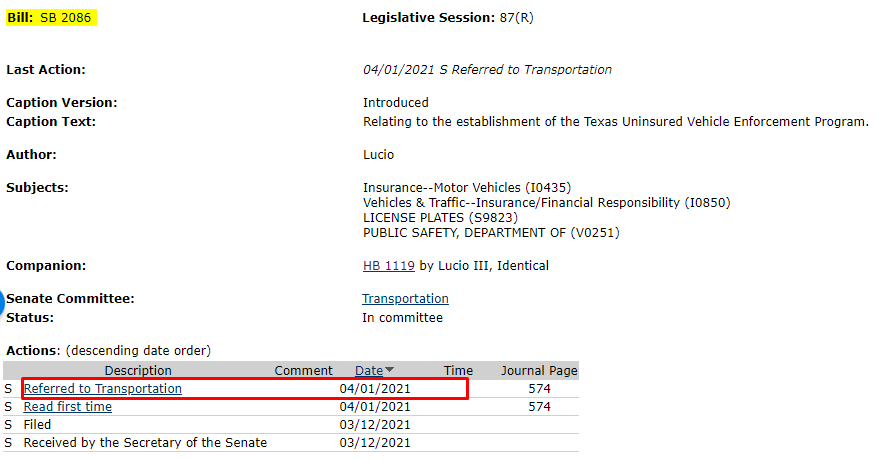

An identical bill was filed in the Senate, and it was just recently referred to a Committee on 4/1:

Source: Texas Legislature Online

In other words, the Texas bill has a long way to go before being signed into law:

Source: Texas Legislature Online

Which is a problem – the Texas legislative sessions ends on May 31, 2021, IN JUST FIVE DAYS, and doesn’t reconvene until 2023, making it extremely unlikely that REKR wins the Texas business anytime soon.

On the 1Q21 earnings call, Berman told investors that “In Texas, we still don’t know what is happening, as there are few more weeks of sessions out”:

Source: 1Q21 earnings call

We firmly believe that Berman’s statement is at best unaware of the timeline we’ve presented, or at worst misleading to investors. In light of this, we asked REKR when they expected to know whether the Texas bill would go through – REKR’s EVP Charlie Degliomini responded by asking about our employment and stated that “Much of what you are asking for beyond what is in the Q is material non public information.”

And let’s assume a bill does make its way back in the 2023 session – similar proposed regulations have fared poorly in Texas:

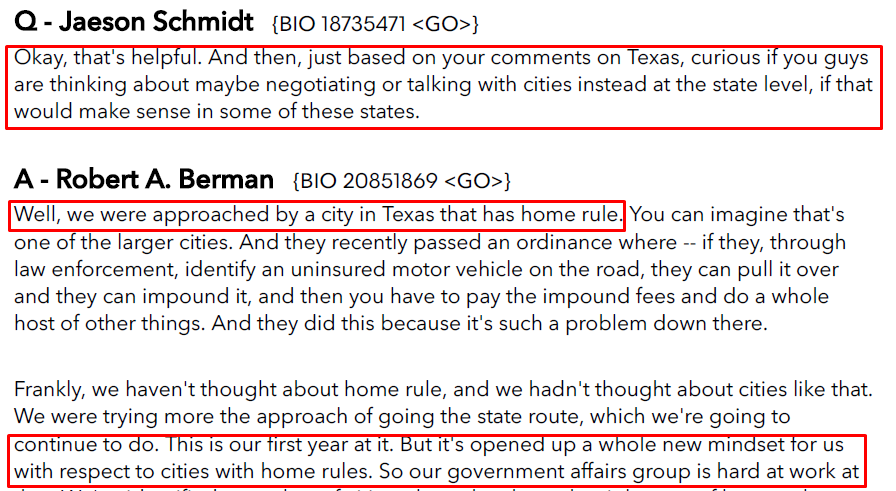

- In 2016, AG Ken Paxton “turned down a proposal to deploy automated license plate readers (ALPRs) across Bowie County in an attempt to ticket motorists with lapsed insurance”. This is especially relevant given Berman’s comments on the 1Q21 call about “home rule”:

Source: 1Q21 earnings call

In Paxton’s denial to Bowie County, he noted that counties only have powers granted by the Texas Constitution and Legislature, and no statute authorizes the use of “automated photographic or similar technology”:

Source: Paxton letter to Rochelle

- In 2019, Texas Governor Greg Abbott banned the use of red light cameras in Texas, citing, among other issues, constitutional rights:

Source: GregAbbott.com

The fact pattern for Texas and the other states makes it unlikely that REKR will gain much traction outside of Oklahoma.

In our next sections, we illustrate our belief that REKR’s largest 2020 revenue contributor will be down 95% in 2021 and our concerns with management and REKR’s auditor.

We show that REKR’s largest revenue contributor in 2020 is unlikely to repeat

In 2Q20, REKR reported that its $1.2MM increase in sales year over year was due to “the implementation of a large software and hardware contract in Florida which generated up front revenues from building infrastructure.”

Similarly, in 3Q20, REKR reported that its $590k increase in sales year over year was due to “the implementation of a large software and hardware contract in Florida which generated up front revenues from building infrastructure.”

Both filings note that in March 2020, REKR signed an “agreement with the City of Lauderhill [which is in Florida] for $1.79 million and contract to provide services for a five-year term.” This amount is corroborated by a bid result summary from the City of Lauderhill:

Source: City of Lauderhill

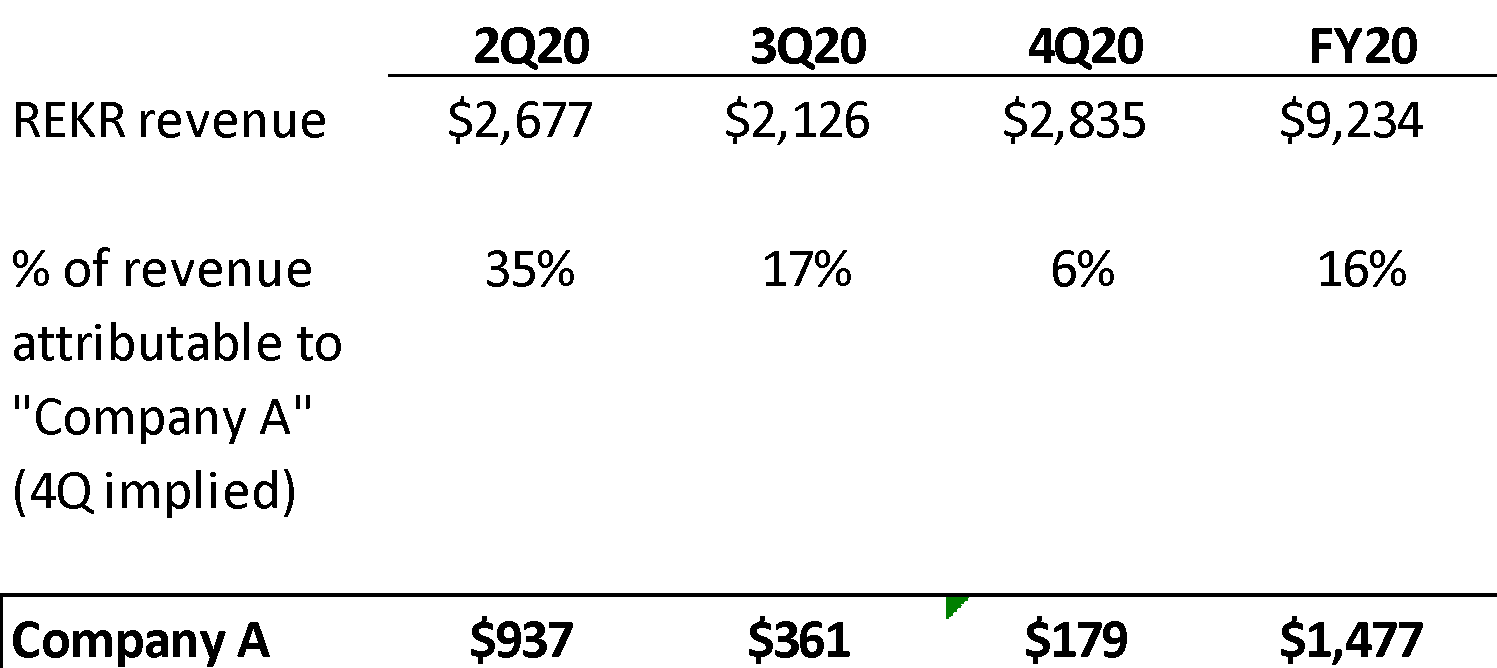

REKR provides a customer concentration analysis in the 2Q20 10-Q, the 3Q20 10-Q, and the 2020 10-K that shows that a “Company A” was responsible for approximately $1.5MM in revenue through the year:

Source: 2Q20 10-Q, 3Q20 10-Q, 2020 10-K

Based on the timing of the Lauderhill contract (March 2020) the two mentions of a “hardware contract in Florida” in the two 10-Qs, and the size of the revenues, we think that Company A is the City of Lauderhill. Assuming that, we believe that REKR recognized $1.48MM of the five-year contract value of $1.79MM, or ~83% of the contract, in 2020.

This means that the remaining $313k, if recognized ratably over the next four years, will contribute just ~$78k annually – implying that the Lauderhill contract revenues will be down almost 95% in 2021 and REKR will have to dig up well over $1MM in revenues in 2021 to make up for the non-recurring nature of this contract.

Curiously, another “Company A” shows up in the 1Q21 results – this time accounting for 40%, or $1.69MM of the $4.22MM in total revenue. This is another large concentrated source of revenue that could be non-recurring. We asked REKR for further detail on Company A, and what % of REKR’s total revenue base is recurring – REKR’s EVP Charlie Degliomini responded by asking about our employment and stated that “Much of what you are asking for beyond what is in the Q is material non public information.”

We highlight Lauderhill to show investors that a meaningful part of REKR’s revenues have been non-recurring, and as a result REKR’s revenue base is likely not as predictable as investors might think.

Governance issues as a further cause for concern

If a fragmented revenue base consisting of relatively small ticket clients is not enough of a concern to investors, we think that REKR’s management and auditors provide additional cause for concern.

In well researched piece by Western Edge, we learned about the following:

- REKR allegedly purchased a business from a childhood friend of CEO Berman

- An auditor resignation after being allegedly threatened with litigation by company executives

- Significant management turnover

Adding to this, we have concerns about both REKR’s CFO and COO:

- REKR’s CFO, Eyal Hen, previously spent 11 years at Ormat, leaving in 2015 as VP of Finance and Corporate Services. Hindenburg Research recently wrote a damning piece on Ormat’s allegedly corrupt dealings in emerging markets that occurred during Hen’s time there. Ormat itself recently disclosed that it is “providing information as requested by the SEC and DOJ related to the claims”

- REKR’s COO, Rod Hillman, was co-founder of a reverse merger known as Game Trading Technologies, which filed for bankruptcy in 2012

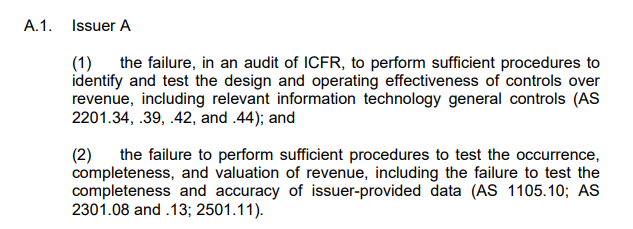

In 2019, REKR switched auditors to Friedman LLP, making it, until a few days ago, Friedman’s largest publicly traded client.

The PCAOB appears to have found numerous deficiencies in Friedman’s audit work over the years:

- A 2018 inspection found deficiencies “of such significance that it appeared to the inspection team that the Firm, at the time it issued its audit report, had not obtained sufficient appropriate audit evidence to support its opinion that the financial statements were presented fairly.” These deficiencies were as follows:

Source: 2018 inspection report

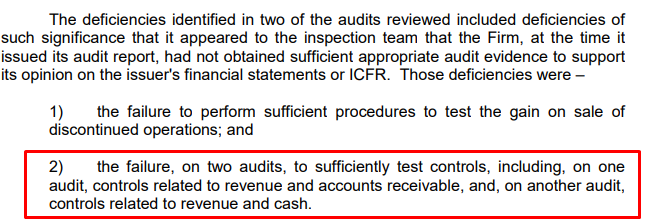

- A 2012 inspection found other revenue related deficiencies:

Source: 2012 inspection report

We believe that in addition to what appear to be optimistic revenue expectations and statements, the issues revealed in the Western Edge report, combined with the history of REKR’s CFO and COO and the audit deficiencies should cause investors to cast a jaundiced eye not only on the REKR’s ability to grow revenues but also on the credibility of the REKR’s management team and their statements.

Valuation and conclusion

The Mariner Instant Replay:

- Public filings suggest that REKR’s Oklahoma contract will, at best, be a sub $2MM revenue opportunity, approximately 96% below CEO Berman’s intimations

- Contracts and press releases imply that REKR’s “largest” contracts are much smaller than investors think, and make reaching optimistic sellside estimates unlikely

- A number of failed legislative efforts suggest that REKR is unlikely to gain traction in other states, and that the Texas bill will amount to nothing

- It appears that REKR’s largest revenue contributor in 2020 will be down ~95% in 2021, and that REKR’s revenue base is not as recurring as investors may think

- We think that REKR’s history as covered by Western Edge Research and the auditor issues revealed in this note should cause investors to question the company’s credibility

In light of all of this, it is our view that sellside estimates of $26MM in revenue in 2021 and $53MM in 2022 are way too high and perhaps pipe dreams at best.

We don’t believe that REKR will do more than $10MM in 2021 in the best case – this means that REKR currently trades at ~38x our $10MM estimate. Assuming the highest multiple in a comp set comprised of similar businesses, we arrive at a price target of $3.71, down ~68% from current levels: