Portfolio manager summary (Idea originally posted May 4, 2020)

- Homology (FIXX) is a gene therapy company whose technology has been criticized by scientists as “untrue to the scientific community”

- On April 15th, 2020, a key patient in FIXX’s only Phase 1/2 clinical trial shared test results on Facebook that suggest FIXX’s HMI-102 gene therapy is unlikely to be efficacious

- In response, FIXX stock fell almost 25%, and instead of providing all investors with an update, management quietly updated the sellside, stressing product safety but not efficacy

- In light of this result, we believe that the HMI-102 trial will not reach its primary endpoint, and that the stock should trade to cash value, or $5.80 per share

- Social media is important – early stage drug company Allakos also had trial revelations posted to FB – the exposure of these led the stock to fall over 50%

Executive summary

It’s an understatement to say that Facebook has changed the world – it’s created an ability for people to be transparent about their experiences, lives, and opinions, for better or worse. In the case of Homology, it’s for the latter. Homology, a gene therapy company whose technology has already been scrutinized by scientists as “untrue,” has just one product in clinical trials, HMI-102, for the rare disease phenylketonuria (“PKU”). As Med Genie reported back in January, FIXX’s trial update showed interim phenylalanine (Phe) results that suggested HMI-102 was not efficacious for low and mid-dose patients.

Our note highlights a data point the company would very much like you not to know – the only patient in FIXX’s high dose cohort posted her results on Facebook, and they show that HMI-102 is unlikely to reach trial endpoints even at a high dose. We believe this patient was forced to take her posts down as a result, and management selectively disclosed the issue to the sell side, providing comments about the drug’s safety, and conveniently ignoring the implications to efficacy and the business. Maybe they were hoping to raise capital before officially announcing trial results. Who knows? We believe that the HMI-102 program is dead in the water, and since its progress is the major driver of FIXX’s value, we believe that the stock should trade to cash value, or $5.80, down 56% from the April 27th close.

Background

The best shorts are often one-trick ponies, but rarely do we find one where a single data point completely upends the long investment case. Homology Medicines, FIXX, is one of those rare finds.

Homology is a gene therapy company which has their first and lead product candidate, HMI-102, in a dose-escalation Phase 1/2 trial (pheNIX) for phenylketonuria. FIXX also has 2 IND-enabling programs and some discovery stage programs, but the HMI-102 trial is the company’s main shot at viability.

PKU is a relatively rare disease, with a U.S. incidence of approximately 350 cases per year and a prevalence of just 16,500, per FIXX’s 10-k. PKU is tied to mutations in the gene that control PAH, an enzyme that metabolizes phenylalanine, or Phe. The condition results in a deficiency in the enzymatic activity of PAH, causing an excess in Phe in the bloodstream that can result in intellectual disability. PKU patients are identified soon after birth, and are primarily treated with a Phe-restricted diet. FIXX’s HMI-102 seeks to modify the underlying genetic cause of PKU, effectively curing the disease and allowing patients to eat normally and not experience the cognitive and metabolic issues from higher than normal Phe.

FIXX’s technology, which does not use the CRISPR approach to gene therapy, has already been subject to scrutiny, with David Russell, a researcher at the University of Washington, saying, “What’s surprising is this company raised so much money on something thought to be untrue in the scientific community,” in a piece in MIT Technology Review.

We believe that recent revelations about the efficacy of HMI-102 support this skepticism and show that the drug is not efficacious, kicking out the one leg holding up FIXX’s business, and that FIXX should trade to cash value, or $5.80 per share, down 56% from the April 27th closing price.

The pheNIX trial

The pheNIX trial for HMI-102 launched in June 2019, and its primary efficacy endpoint is two plasma Phe measurements below 360 umol/L (or 6 mg/dL) between 16 and 24 weeks after dosing. Following evaluation of the first two patients in a cohort, “a decision can be made to either escalate to the next dose level, add a third patient or expand the cohort at the selected dose level”.

Now before we review what’s new, it’s helpful to note that a mouse study presented at the 21st Annual Meeting of the American Society of Gene & Cell Therapy titled “Sustained Correction of Phenylketonuria by a Single Dose of AAVHSC Packaging a Human Phenylalanine Hydroxylase Transgene” showed that HMI-102 showed an effect to mouse Phe levels just one week after dosing – in fact, mouse Phe levels remained relatively flat after that first drop.

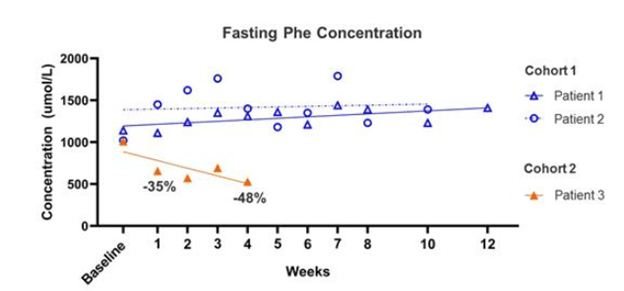

This would imply that the therapy shows its effect soon after dosing and the longer timelines contemplated in the study endpoints are to indicate that the effect is long lasting. Sure enough, we see a similar dynamic in the pheNIX trial data released by FIXX in December 2019. There were 3 patients examined here – from the 10-k: “(n=2 patients in the low-dose Cohort 1 and n=1 patient in the mid-dose Cohort 2) as of the data cutoff of December 2, 2019. A fourth patient was dosed in Cohort 2 subsequent to the data cutoff date and was therefore not included in the analysis.”

In this release, we see the two patients in the low-dose cohort experienced no improvement in fasting Phe after dosing or even 12 weeks later. The cohort 2 patient, getting a mid-dose, showed an improvement in Phe level immediately after dosing, but their Phe level did not fall below the 360 umol/L threshold defined as the primary endpoint (it stayed around 500) calling into question the efficacy of the treatment, which Med Genie mentions in their piece (from the 10-k):

Damning revelations

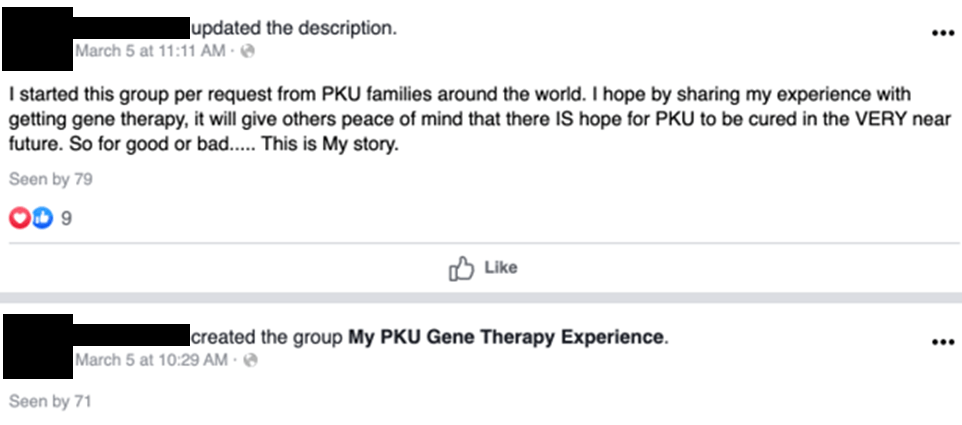

On March 5, 2020, a woman we will call Miss A started a Facebook group (since made private or taken down on April 15, 2020) to discuss her experience getting gene therapy for PKU:

On March 9, 2020, Miss A, who lives in Normal, IL tells us she’s going to Chicago, which happens to be one of the pheNIX trial sites:

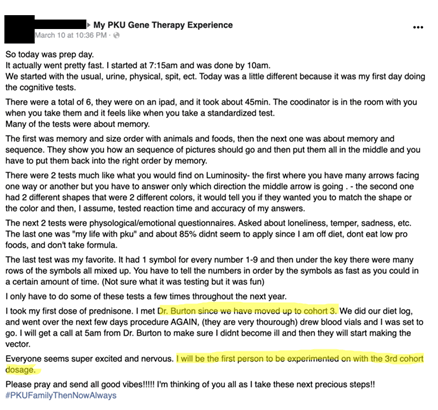

The next day, Miss A provides us with enough to data to know that she is Patient 5, part of the high dose cohort 3 in FIXX’s HMI-102 trial (cohort 3, mentioned by Miss A, would be the next dose up from the cohort 2, the mid-dose cohort):

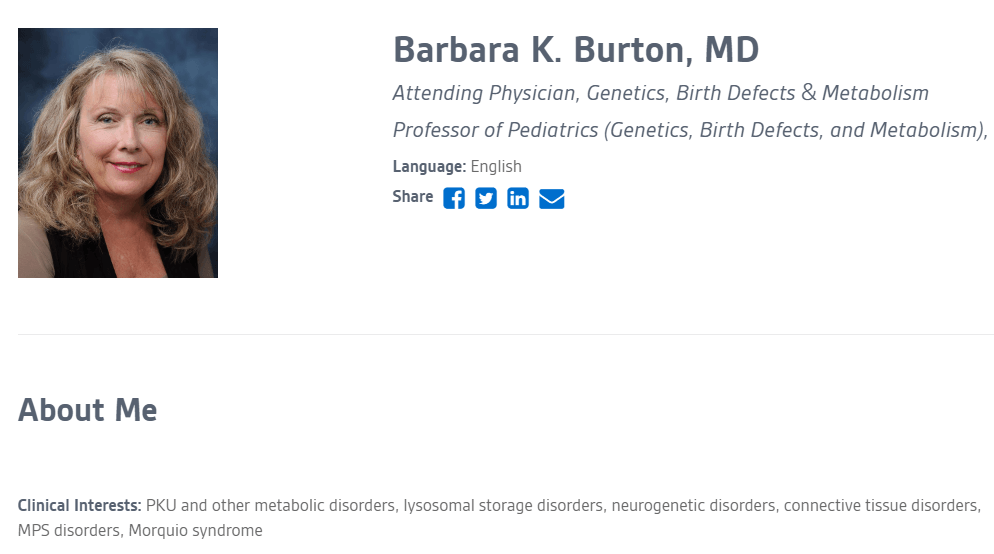

Dr. Burton appears to be Dr. Barbara K. Burton, a physician focused on PKU at the Ann & Robert H. Lurie Children’s Hospital of Chicago, a trial site mentioned in the pheNIX trial description on clinicaltrials.gov:

This, taken together with the fact that Biomarin’s own PKU trial was in too early a stage to enroll a Cohort 3 patient in March 2020, it’s probably safe to say that Miss A is taking part in FIXX’s pheNIX trial.

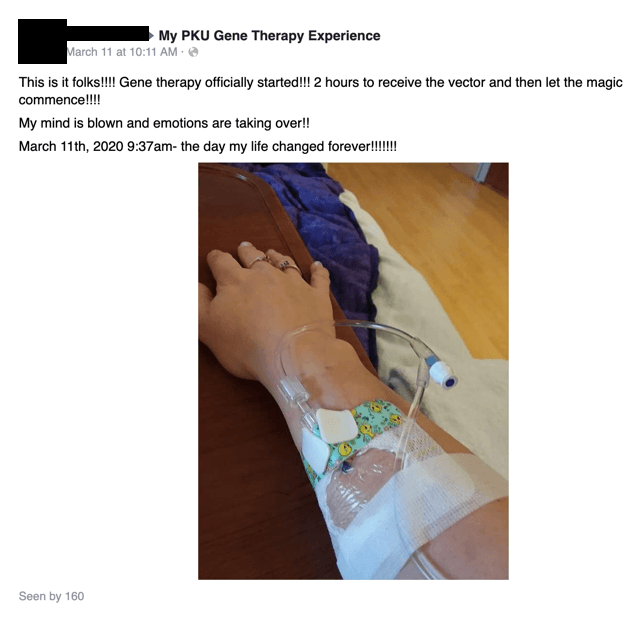

On March 11, Miss A receives her infusion:

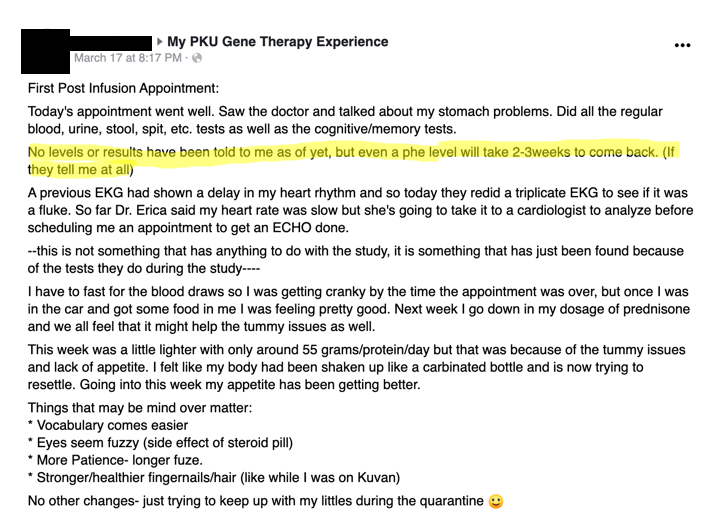

Miss A then shares a series of updates on how she is feeling and the progress of her weekly visits post-infusion. Six days post infusion, she says she hasn’t gotten any test results back, but that it may take 2 or 3 weeks to get a Phe level:

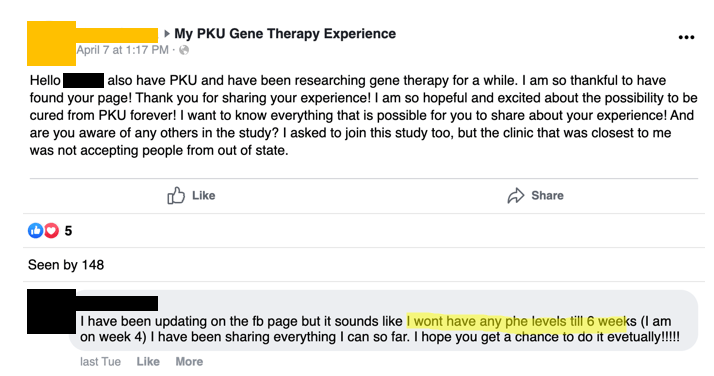

27 days post-infusion, Miss A tells a FB commenter that she won’t get Phe levels till six weeks post-infusion:

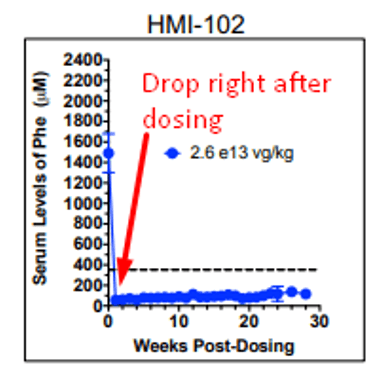

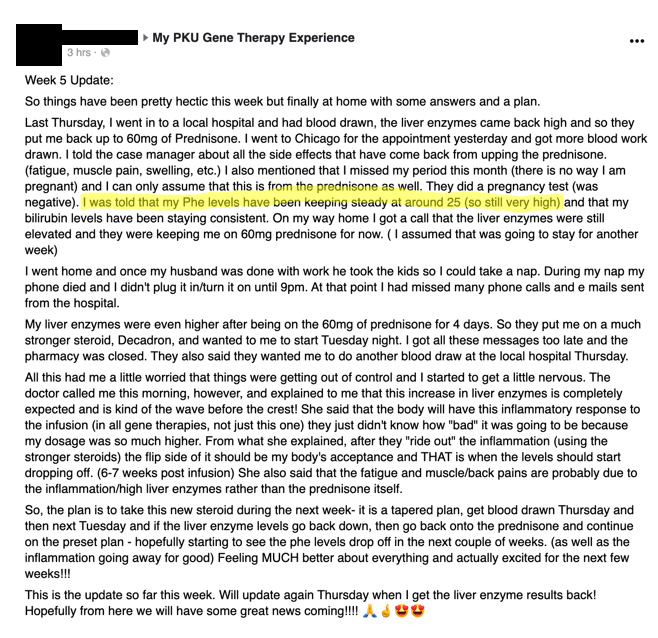

And then 35 days post-infusion, on April 15, 2020, a bombshell – Miss A gets her Phe levels, and at 25 mg/dL or 1497uMol/L, they are well above the 360 uMol/L endpoint threshold after 5 weeks (and after the drug typically takes effect), suggesting that HMI-102 is not efficacious even for a high dose patient:

Just a few hours after her post, Miss A’s entire group is either taken down or made private, perhaps at the demands of FIXX itself.

Management’s disclosure problem

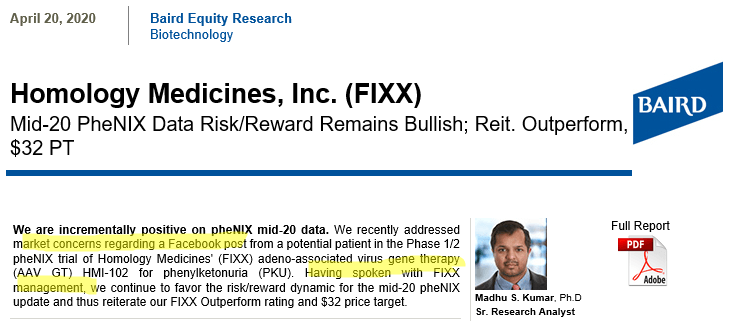

We believe that management was aware of this post and tried to manage the perception of it by talking to the sell side and to select investors. In fact, Oppenheimer’s equity sales desk was sharing the below email conversation between their analyst Matt Biegler and FIXX’s Theresa McNeely to explain the price action on April 15th:

Who was Theresa planning to speak to? We know that Baird’s Madhu Kumar got a call:

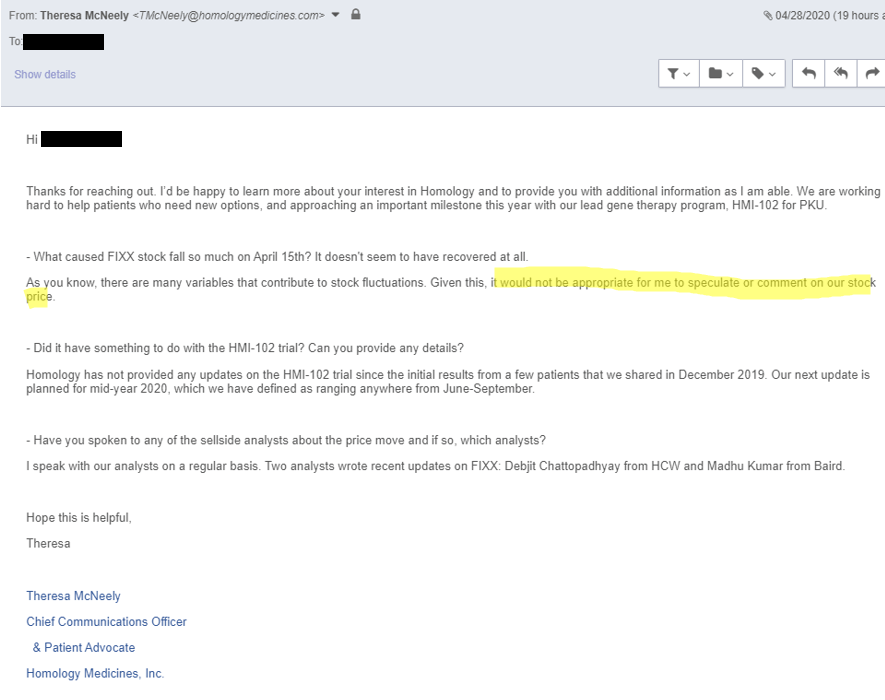

But when we asked Theresa ourselves, she was much less forthcoming:

It appears to us that FIXX chose to inform the sell side and potential larger investors, who appear to be selling the stock (it has dramatically underperformed biotech broadly), but not the average investor. This is a significant red flag that investors should be aware of.

Why all this matters

Because the mouse study and the Cohort 2 data showed an effect to Phe levels one week after dosing rather than a gradual reduction, we can conclude that Miss A’s level, at 1497 uMol/L, is probably not going to get better, unfortunately. Further, her levels several weeks into the trial are still much higher than the threshold level specified in the primary endpoint of 360 uMol/L. This means that the therapy is showing zero efficacy even for a high dose patient. This data point is damning given the size of the trial and importance of the high dose patient in light of the lack of efficacy in the low and mid-dose cohorts.

Now the sell side may parrot management and say that there is no way to know whether Miss A is who she says she is, but the evidence is certainly strong supporting her case. They may say that there was no way for her to know her Phe level, but her posts show that she expected to receive them. They may also say that the drug is safe, and that liver enzyme elevation should be expected in a therapy like HMI-102, but that’s all beside the point. The point is that the Phe level Miss A received 5 weeks after infusion show that HMI-102 is not efficacious.

These results support the skepticism around FIXX’s use of the AAVHSC vector in liver directed gene therapy, which, based on the results thus far, and in particular Miss A’s results, appear to show zero efficacy and thus makes it inferior to Biomarin’s AAV5 vector.

Furthermore, if management thought this information was material enough to talk to the sell side analysts covering the stock, why not put it in an 8-k or even a press release for the benefit of their entire shareholder base? Given the materiality of the information, wouldn’t all shareholders have benefited from the same level of disclosure rather than be kept in the dark? This is behavior consistent with that of MDXG and ALLK, both companies with executives formerly from reputed companies who have seen their stock prices demolished.

For FIXX, we believe that this is a huge problem – the HMI-102 pheNIX trial is the ONLY program in their portfolio that is in the Phase 1/2 stage, and thus the primary path to viability for the company. With this piece of data showing that HMI-102 is not efficacious, we believe that the program is likely worthless and unlikely to proceed to commercialization. While FIXX may try to apply HMI-102 to other indications, we believe that doing so would essentially restart the trial and approval clock without making up for the lost time to market from a failed PKU trial.

Furthermore, social media matters. While FIXX management may be dismissive of people posting on Facebook, these posts have value. In the case of Allakos (ALLK), Seligman Research put together a barn burner of a report which included numerous Facebook posts questioning the efficacy, safety, and trial design of ALLK’s drug candidate. Since that report, ALLK stock is down approximately 51%, and ALLK actually has several later stage trials.

In the case of FIXX, we believe that HMI-102 in PKU is the ONLY path to viability – given the lack of efficacy of HMI-102 at high dose, we believe that the HMI-102 program is dead, and that the stock should trade to its cash value per share, or $5.80 per share, down 56% from the April 27th close price.